An Insurer that ticks our boxes

Peter Reed, PPM Portfolio Manager, discusses the evolving landscape of insurance and the positive investment story resulting from the concentration of market participants and premium growth.

Insurance is fundamental to any properly functioning, modern economy and we are always open to investment opportunities within the sector when the occasion arises.

By way of diversion, it is interesting to briefly review the history of this industry, a fascinating story in its own right. The modern insurance industry dates back to the late 14th century when merchant bankers began to separate marine insurance contracts from debt financing contracts. That is, separating credit risk from peril risk, thereby reducing the cost of both.

Thus, insurance originally evolved as a commercial instrument; it was not until after 1666, as a result of the Great Fire of London, that insurance for households – Fire Insurance – emerged. The aftermath of the Great Fire actually saw the creation of the first insurance company, The Insurance Office, in 1667. What happened to The Insurance Office is unknown, but the oldest documented insurance company still in existence started life as a fire office: Sun Fire Office, now known as RSA, is one of the largest insurers in the UK.

Perhaps explaining the development and success of the industry over the centuries is the real benefits provided by the industry. At the macro level the industry helps efficiency and resilience of the economy by facilitating the transfer of risk. At the micro level it helps minimise the impact of unexpected events and helps people organise lives with greater certainty. For example, people would not be prepared to invest most of their wealth in a single house without insurance, thereby supporting the private housing market.

Not unlike the Australian banking industry, we have long considered the general insurance industry to be attractive from a structural point of view.

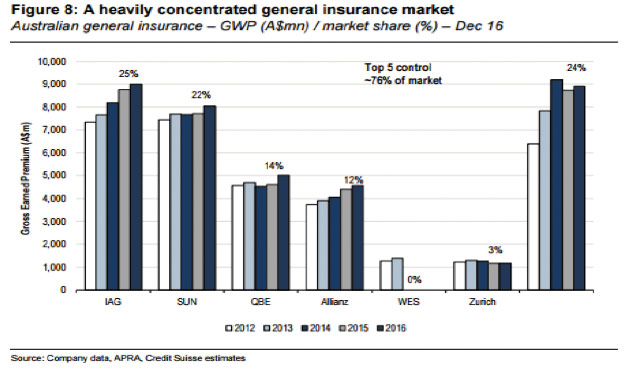

The top 5 insurance providers control around 76% of the market with the top two, IAG and Suncorp combined, comprising just under half.

This structure has helped produce acceptable growth in premiums over the long term. Although the industry has a cycle, focused particularly around large event losses, premium growth over a 20 year period has been around the 4% per annum level.

These are the underpinnings of what could potentially be an attractive opportunity for long term investors.

Homing in on IAG, the largest Australian general insurer, the company has been well managed over a long period of time, in our view, and most recently under Mike Wilkins took the CEO role in 2008.

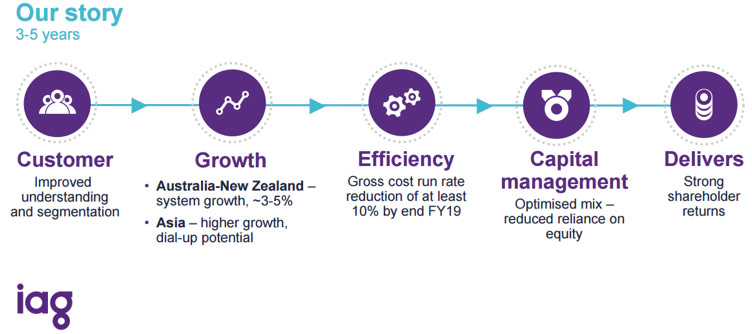

Further, management have detailed a clear strategy over the next 3-5 years which should deliver attractive, above-market growth over this time.

This strategy has a number of components, each providing a level of confidence in the investment proposition. First is the top-line growth outlook of 3-5% – in line with the long term experience. Our view is that this is quite achievable given the elevated level of claims experienced by the industry as a result of weather events and the need to rebuild profitability and capital.

Cost out, or efficiency opportunities, provide an additional level of confidence to the investment story. IAG management have highlighted this as a key goal, thereby indicating a high level of belief in their ability to achieve at least a 10% reduction in the cost base. Further, we would suggest that competitors Suncorp and QBE have, of late, led IAG in this endeavour, highlighting the opportunity for IAG.

The final leg to the IAG investment thesis lies with its strong capital position. Currently, the company holds 1.8x its required regulatory capital amount – above its target of 1.4-1.6x. Capital generation from earnings growth in addition to the benefit the company received from a so-call quota deal with US insurer Berkshire Hathaway which will result in a reduced capital requirement of approximately $700 million over the first five years of the transaction.

We envisage the company having increased capacity for higher returns being made available to shareholders over the coming years.

Each of these points is important in their own right and together, in our view, present a compelling investment case for IAG.

By way of note, IAG and Berkshire Hathaway have had a successful reinsurance relationship since 2000. The 2015 deal between the two companies, labelled as a strategic partnership, partly involves Berkshire taking a 3.7% stake in IAG in addition to a quota share arrangement. The quota share is a 10 year deal where Berkshire receives 20% of IAG’s consolidated gross written premium and pays 20% of claims. Crucially, Berkshire will also reimburse IAG for its share of operating costs and pay a percentage-based fee which recognises the value of accessing IAG’s franchise.

The benefit to IAG is that it will diversify the company’s funding whilst also delivering a more stable income stream with fee income replacing volatile premium income. Further, the quota share arrangement will result in a reduced capital requirement for IAG of approximately $700 million over the next five years. In so doing the company expects the deal to enhance its ability to deliver a through-the-cycle 15% return on equity.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. ©Copyright 2017 Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Print this Article