A Return to Normalcy

After a significant re-adjustment of valuations over the last year, we feel that a wide range of stocks are now attractively priced. Actions to lower inflation should not cause more than a mild recession, something that has already been assumed in prices. Capital markets return to more normal conditions after a decade of distortion from near zero interest rates.

In an economic sense the most significant event in 2022 was the rapid rise in inflation and the equally rapid increase in interest rates by central banks in developed countries. It was the first time in 15 years that interest rates have increased significantly. The current levels are not high by historical standards and represent only a very modest margin over the “target” inflation rate.

A corollary of zero interest rates was that asset valuations became highly inflated. This was particularly the case in the technology sector which subsequently came under severe pressure. Many market darlings dropping 50% and some of the “unicorns” declined 80-90% or more. Companies in mature industries where valuations were less carried away did not suffer much or even went up.

Operating result for companies to date have showed resilience in the most part. However, fears of recession resulted in prices of companies perceived to be exposed were marked down. We would re-iterate the observation, made in the last article, in early December, that bad or extended economic downturns tend to be associated with financial crises – usually bank crises.

This was most recently the case in the GFC when lack of availability of bank lending hindered economic recovery.

This is not the case now and the bank sector is in rude good health. Lending has been conservative for many years, particularly leading up to the Hayne Commission. Bank balance sheets are very healthy and capital ratios are strong. There should be no impediment to the bank sector supporting the economy.

We feel that the current inflationary situation is a different order of magnitude to that of last major outbreak in the 1970s. At that time a number of attempts were made to quell the outbreak culminating in the draconian actions of the Federal Reserve under Paul Volker. On this occasion inflation was caught a lot earlier and two of the factors that have driven it seem to be abating already:

- Supply chains which were severely disrupted by the Covid have largely re-opened.

- Commodity price jumps caused by the Ukrainian war have retreated very substantially.

A remaining problem is shortages of labour and resulting increase in wage pressures. This is currently the subject of intense scrutiny.

There is widespread expectation of further increases in interest rates in the next six months although it is thought that the increases will moderate and settle at a slightly higher level than the present.

Our view is that the tightening will lead to a slowdown rather than a severe period of economic difficulties such as occurred during the GFC. None of the excesses of that period have occurred. The real estate boom we have seen has not resulted from wild bank lending and speculation in real estate. Rather the increase in house prices has been more as a result of shortages of housing, something that is also the case in the US and the UK. The significance of this is that there is not a backlog of inventory to be disposed of and a collapse in construction. The unfilled demand remains.

The market valuations having already declined significantly we feel that many companies represent good value. This extends to companies in the construction industry such as James Hardie and other beneficiaries like Harvey Norman. Quality retailers such as JB HiFi are also attractive.

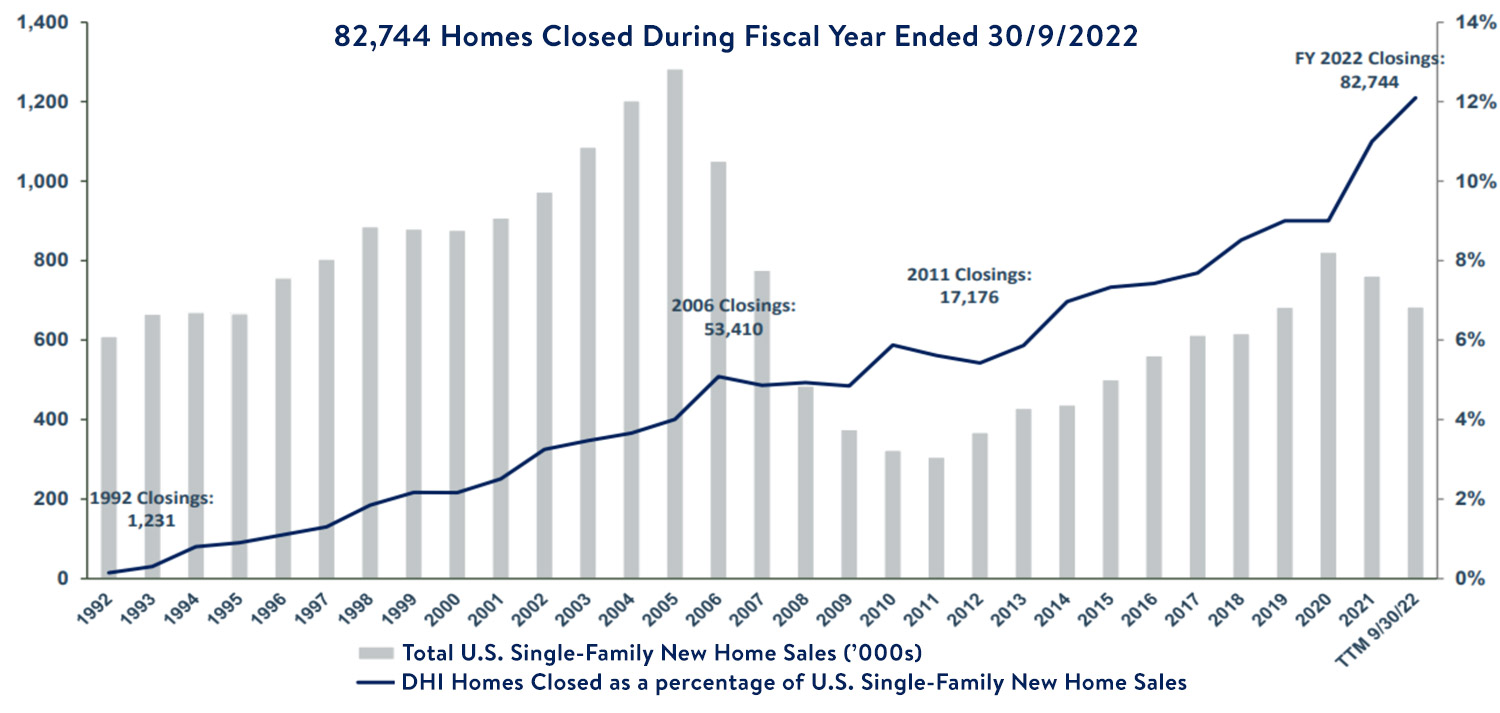

It is significant that the US home builder DR Horton, which builds about 12% of the country’s single-family homes, has risen 50% from the lows of 2022. The chart below shows the number of homes built in the US over the last 30 years. The number of homes built in the recent past is below the long-term average and the average of the last 10 years is very low and has resulted in a shortage. A similar pattern exists in Australia and a number of other developed countries.

Source: DR Horton Q4 2022 Report

For further information on Private Portfolio Managers Pty Limited (PPM) and our service offering please contact Jill May, Head of Client Relations or your Portfolio Manager on (02) 8256 3777 or jm@ppmfunds.com