Bonfire of the Volatilities

LESSONS AND OPPORTUNITIES POST-GFC CONTINUE

A discussion of PPM’s views by Peter Reed, Director/Portfolio Manager at Private Portfolio Managers

It’s fair to say that the makeup of PPM’s holdings of financial stocks has changed significantly over the past decade or so.

Around the time of the GFC exposure was dominated by the major Australian trading banks. Loan growth remained healthy: this was particularly the case with residential mortgage lending where borrower debt levels were not excessive and house prices (at least in hindsight) had not moved into unreasonable territory.

For a long time we had been attracted to the sector partly because of the appealing structure of the industry in Australia. Residential property lending was dominated by the big-4 banks and this position was further strengthened post-GFC as the smaller lenders lost competitiveness against their major rivals.

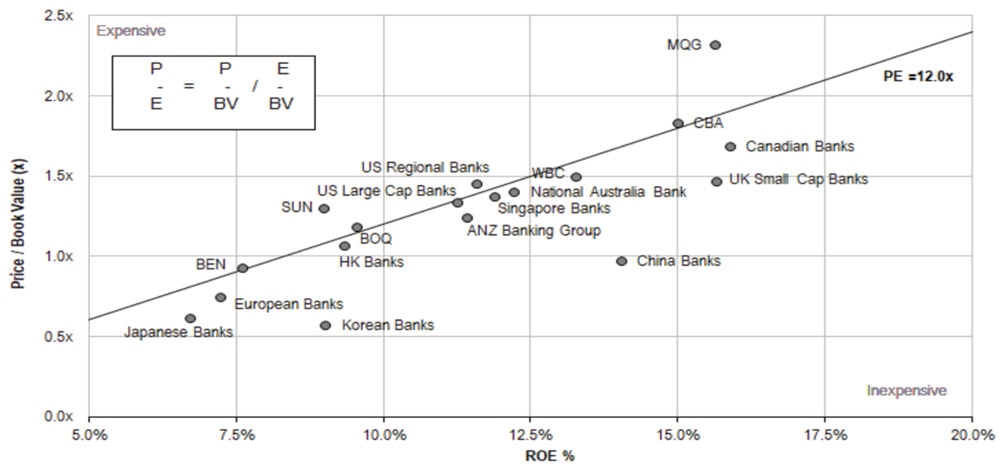

But as these cycles typically work out, asset (house) prices soared, borrower indebtedness continued to rise and the skew of the banks’ exposure to this segment continued to rise, all of which gave rise to concerns over risk levels of the banks and the outlook for growth. Although bank lending books remained healthy, at least in terms of bad and doubtful debts, we did not have to think too hard to come up with scenarios where what appeared solid loan books quickly turned mushy.To reinforce this view, valuations of the banks had been pushed to levels that made them look increasingly unattractive, particularly from a global perspective.

In the case of CBA, for example, the price to book ratio had been pushed above 2X (see chart). When the stock was trading on an ROE greater than 16% this could be justified but at the same time we viewed the risk to the sustainability of such high ROEs as significant. A slowdown in lending growth, higher bad debt experience and a higher regulatory burden, a real risk post GFC, were all realistic possibilities which would affect the ROE.

“At PPM we become particularly interested in banking investment opportunities around a financial or economic crisis.”

It is at such times that with a bit of fortitude investors can buy banks on price to book ratios closer to 1X and, depending on the severity of the crisis, even less than 1X. Remembering that a value of less than 1 indicates permanent damage to the bank’s franchise, if we take a contrary view that there actually remains real value inherent in the franchise then a purchase at such levels, all else being equal, should be attractive.

And so it was from this perspective that with the effects of the GFC rippling around the globe we cast our net further afield for attractive banking franchises which, in our view, appeared attractively valued.

The first port of call in this quest was the US, where unlike Australia, a number of significant financial institutions went to the wall, starting with Lehman Brothers, and many that didn’t were put under severe stress. In such circumstances the sector as a whole tends to suffer a significant market downgrade. This was the case for Wells Fargo, a bank we held in high regard prior to the GFC but which could be argued was ultimately a beneficiary of the crisis.

With the US government looking for relatively strong institutions to help bail out weaker competitors, Wells was the prime contender to step up and take over Boston-based Wachovia Corp. Matched with Wells’ west coast centred business, the combined banks now offered a true coast to coast banking franchise with 9,000 branches and over 12,000 ATMs.

At the same time most other major competitors of Wells, having been put under severe financial pressure, were now distracted with the prime task of remediating their own business – writing off bad debts, cauterizing parts of the business by creating “good bank”- “bad bank” loan books and generally rationalising the business and slashing costs. The environment was ideal for stronger competitors such as Wells to cement their market position.

Purchased at a price close to book value, our expectation was that over a period as financial markets normalised and assuming the bank is able to further develop its business the price multiple for the franchise will further expand. So not only will the share price likely rise with the natural growth of the business, the valuation multiple applied to the business will also increase as investors become increasingly comfortable with its prospects. This will likely play out over many years and, notwithstanding the occasional difficulty along the way such as the recent issue of regulatory fines against Wells, the investment for our clients is expected to yield attractive returns.

In ensuing editions we plan to look at our experience with bank investments in the UK, again at around the time of great market dislocation following the GFC.

PRINT THIS ARTICLE