Disney goes direct

A discussion by Franklin Djohan, Portfolio Manager of Private Portfolio Managers

A discussion by Franklin Djohan, Portfolio Manager of Private Portfolio Managers

Content and Distribution Wars or an astute progression?

On the surface, there seems to be a power struggle between the studios and content distributors. Apple is the most recent technology company to invest in original content. The budget set aside to produce original content for Streaming Video on Demand (SVOD) companies is not insignificant. Netflix, the pioneer in streaming services, spends around $6 billion a year to produce its own original content. Amazon is not far behind with a budget around $4.5 billion, and Apple around $1 billion.

So when Disney announced that it will pull out some of its content from Netflix and launch its own streaming service, one could be convinced that their relationship has been reduced to tit-for-tat, and it seems that there is an element of that. Obviously, as Netflix gets bigger, the balance of power tips over to its side. To make matters worse, streaming services also encroach deeper into content production. Traditional studios are definitely feeling the heat.

Restoring the status quo, however, is not the sole reason why Disney is planning to launch its own streaming service. The mind-set is different. Netflix, being a technology company, produce original movies and TV series as to differentiate themselves in order to attract subscribers to its platform and retain them. On the other hand, for traditional studios like Disney, it is all about maximising the monetisation of its content. Disney is largely agnostic to where or how its content is distributed.

As the younger generation are now opting to access content through streaming and cutting-the-cord from cable – one of Disney’s distribution channels – the company need to find a new way to monetise its contents. Launching its own streaming service is one way to do that.

One other advantage of having a streaming service is the effect of becoming closer to the consumers. Netflix has been collecting a lot of data on what its consumers watch. That data is then used to select content that is the most appealing to its subscribers. This kind of data will also be invaluable to Disney.

Even with all the benefits, venturing into a direct-to-consumer model is not an easy task even for a company like Disney. First, by pulling some of its content from Netflix, the company will forego some of their licensing revenue. This is why Disney is hedging its bet, and only launching a streaming service on two of its brands, original Disney Characters and Pixar. While the decision for two other lucrative brands, Marvel and Lucasfilm, still remain pending upon the company’s review.

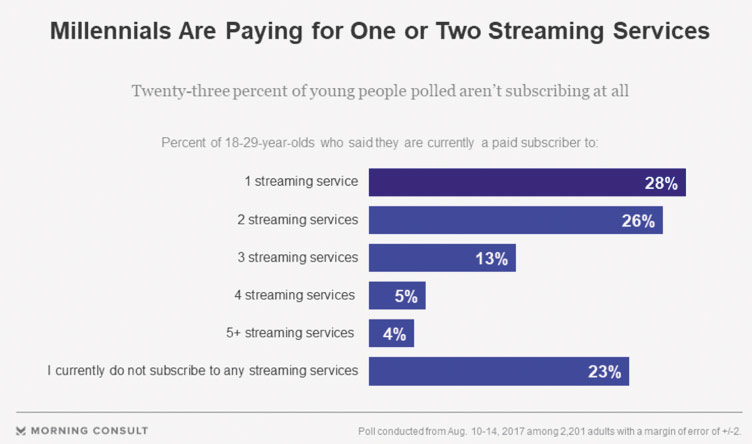

Second, the company will enter into an already saturated SVOD market. Besides the aforementioned big names, there are other streaming services already in the market including Google’s Youtube, Hulu, and HBO Now. Even the Millennials, avid users of streaming services, will have a hard time to subscribe to all of the available SVODs.

Content will play a bigger part, and continue to be the differentiator, amongst the various players.

This is where Disney – who own huge libraries of Intellectual Property from its previous acquisitions of Marvel ($4b), Pixar ($7b), and Lucasfilm ($4b) – will shine. Content is still king after all.

Print this Article