As at December 2021

Equity Market Returns

Source: IRESS

Overview

Equity and property markets ended up strongly over the year. The MSCI, a global equities index, was up 29.3% in A$ terms, the Australian market was up 17.7%, listed property was up 27.0%. The average price of residential property in capital cities was up by 21% as estimated by Corelogic, a research firm. Extremely accommodative monetary conditions, expansionary fiscal policies and continued strength in economies provided support to asset markets.

Cash rates remained unchanged in most developed countries, and those that raised them did so by trivial amounts. Focus however is now on when major central banks will commence raising rates (and cease massive bond buying) particularly in the context of the emergence of inflation, which ended the year at levels not seen since the 1980s. In the US the latest inflation figure was 6.8% and in the Euro area 4.9%. Significantly, bond yields have not reacted having risen barely 0.5% to 0.7%, leaving them well below the headline inflation level. The Australian 10 year bond yield rose 0.7% to 1.6% against our inflation rate of 3.0%.

The Australian dollar was down against the US dollar (-6.0%), the British Pound (-4.7%), and the Chinese Renminbi (-8.2%), but up against the Euro (1.7%) and the Japanese Yen (4.8%).

Generally, portfolios benefited from global exposures as they are invested predominantly in US Dollars and Pounds.

Energy prices rose sharply over the year: oil was up 48% and recently gas and coal prices have increased sharply particularly in European markets. Prices for agricultural products also increased significantly over the last twelve months with food products up 19% and non-food products up 27% (as measured by the Economist indices).

Government Bond Yields

Source: FRED

The inflationary pressures are of sufficient significance that central banks have now decided to “retire” the “temporary” description (it will require more to retiring the size of their bloated balance sheets!) Attempts to predict the path of inflation are not all that fruitful, but the observation that we would make is that fixed interest markets have taken a very benign view of the outcome. Long term yields are down on the highs earlier in the year, and using current data, are at negative real returns of over 5% in the USA. That is, they have assumed the best possible outcome and have built in nothing for any other possibility. Maybe after 30 years of benign conditions (see chart below) it is assumed that inflation is dead.

In earlier commentaries we have observed that ultra-low interest rates are needed to support the extremely high valuations that exist in many stocks (and other assets such as residential property). As we have pointed out previously the main offenders in equities are: technology, luxury goods, infrastructure, renewable energy projects, payments operators (not only the Afterpays, but also Visa, Mastercard etc) and venture capital generally. In this list are many excellent companies, many that PPM has held in the past, such as Mastercard, Microsoft and Alphabet (in larger exposure), LVMH and Hermes. What we are arguing is that it is not the company that is the problem, it is the valuation.

Netflix is perhaps an illustration of the problems that very highly priced tech stocks could face. Netflix came out of the blocks like a bolt of lightning and captured a dominant share of the video streaming market very early. They produced a number of blockbuster series and they also had access to content of traditional studios such as Disney. It didn’t take long for the content suppliers to realise what a threat Netflix was, and they started up their own streaming businesses and cut off Netflix’ access to content. Now there are seven very powerful competitors vying for subscribers and a full-on content war. According to Morgan Stanley, an investment bank, the streaming competitors will spend around $140 billion on content in 2022. Netflix is estimated to spend $17 billion against revenue of approximately $30 billion this year. With a capitalisation of $300 billion Netflix is valued at 10x revenue – with little free cash flow. By comparison, if Verizon, a telco, were to be so valued the capitalisation would be $1,200 billion instead of the current $220 billion. An analogy for the streaming business over the next decade might be the bareknuckle price wars that have gone on in the telco industry for much of the last 15-20 years. Not conducive to over-the-top valuations!

However, excessive valuation does not apply to the whole market and a number of sectors would actually benefit from higher interest rates. In particular, the finance sector, both bank and insurance company margins would benefit from a tailwind if the yield curve rose and steepened. While not benefitting from higher rates per se, sectors such as manufacturing and healthcare are very modestly valued and do not require everything to go according to Hoyle to deliver an attractive long-term return. It could be argued that higher inflation would have a negative effect on their return on capital but the valuations we feel are low enough for this not to be the critical factor.

We’ll give mention of COVID-19 a spell on the bench!

International Equities

International Equities Performance

Source: MSCI

Extremely high levels of capital raisings and excessive valuation of immature businesses were a feature of equities markets again this year. Stocks in fashionable sectors, disruptors of existing business models have been accorded valuation metrics which assume a new paradigm (the pre-cursor to a return to normalcy or lower). The rise in interest rates (on bonds) over the last 18 months, albeit very small in an absolute sense, may be a somewhat dusty canary in a very gassy mine.

In response to our view on the risks of over-valuation, the portfolios have focussed on the price we pay for companies. We think that keeping to values that are not excessive in an historical sense offers the best chance of earning an attractive return on investors capital. The market’s focus on narrative has provided quite a number of opportunities where the story is not liked for some reason, but the numbers look good in a “bond” like way. That is they may not have high top line growth but the return on capital that the investor is accessing is attractive.

The finance sector has not been much liked. Our holdings in US and UK banks have recovered from the lows of 18 months ago but valuations remain at very low levels by historical standards; the same is true of insurance companies. The emergence of slightly higher interest rates is leading to higher returns on their capital, which while still below the levels that they have traditionally earned (making some allowance for the higher levels of capital they are now required to hold) they are nevertheless attractive. Additionally, a simplification of their business models is starting to produce results, after straying into areas not suited to their cultures, capabilities or capital structures that increased complexity and costs. The two main holdings Wells Fargo and Lloyds Banking Group have made progress exiting a scandal strewn period in their long histories. Valuations are yet to catch up with progress as better use of capital and higher margins are starting to appear.

The holdings in telecommunications stocks are attractively valued after a long period when excessive competition reduced the returns throughout the sector. As in much of the technology industries, demand for telecommunications products and services has been insatiable (look at what has happened to one’s data usage and demand for higher transmission speeds). The difference in this industry has been the inability to convert demand growth into revenue growth. However, fights for market share would appear to have subsided in the interest of improving returns (though, like a sack full of cats they might start scratching at any time). The transition to 5G, with its capital requirements has helped bring about the development. Increases in prices we think will result in substantial improvements in returns. Initially we held both Verizon, the largest US mobile operator and AT&T, which was in the process of disposing of its media business, but we have decided to focus on Verizon as the better placed operator and with less debt. High capital expenditure had placed pressure on balance sheets however high cashflows have rapidly reduced the debt burden.

In the healthcare sector we have added Universal Health Services (UHS) to the portfolios. UHS owns and manages acute care hospitals and behavioural hospitals in the US (and a smaller operation in the UK). What we like about the company is the long history of strong returns and discipline in building the network. There have been cost pressures during the last two years as labour shortages have developed. These are expected to abate as nurses return to more traditional employment patterns. The pricing of the stock is very attractive at 11 times earnings.

We retain a reduced holding in two technology stocks Microsoft and Alphabet (and have not bought for new money for over three years). Operationally they have both been performing very well, however the value is becoming increasingly difficult to justify. This is a long way from the situation 10 years ago when Microsoft traded on a valuation more like a telco!

As indicted earlier the current position is one where excesses exist in a number of parts of the market, some of them in extremely attractive companies which under a different pricing regime we would buy, but currently that does not exist and it is time to keep a disciplined approach to valuations.

Australian Equities

Australian Equities Performance

Source: IRESS

The Australian equity market rallied into the end of the year to produce a total gain of 2.48% for the quarter and 17.74% for the year.

COVID-19 disruptions have remained a lingering feature – as I write this note ahead of Christmas, Sydney CBD is almost as quiet as during the major lockdowns earlier in the year and at the beginning of the pandemic in 2021. To date government support measures have largely offset the negative financial impact to individuals and corporates, but we can assume that we have now passed peak fiscal stimulus. Further, we can expect the RBA, in line with other central banks around the world, to gradually move away from its ultra-easy monetary policy. The first step will be a winding down of quantitative easing programs with interest rate rises to come later. Although the rate rises will likely be gradual, at least at the start of the tightening cycle, it portends to a more difficult investment environment in the periods ahead.

Banking stocks were prominent during the quarter with ANZ, NAB and Westpac reporting full year results. The scenario envisaged of a tailwind provided by the write back of provisions taken during the early stages of the pandemic continue to play out and will likely provide a continuing tailwind for the sector. A lift in credit growth as the economy lifts and mortgage and business lending strengthen is another notable factor.

Offsetting this, however, has been a compression in bank net interest rate margins (NIM) as banks have sought to compete aggressively for a slice of the growth. The Australian bank sector is a classic example of an oligopoly structure, typically with low to moderate levels of competition. As the bond market yield curve steepens this normally would allow the banks to increase their NIMs. This has not occurred so far in the current environment, but the industry structure remains tight and we would expect the banks, at some point to focus on their margins.

Further impacting bank profitability has been elevated costs from a mix of inflation, investment spend and compliance expenses. If we assume strong mortgage competition is likely to offset the benefits of a steepening yield curve, we probably need to look to second half FY22 or FY23 to see the benefits from higher business credit growth and an easing in the various cost pressures faced by the banks.

Other portfolio stocks to report during the quarter were Amcor and Orica. We provide detailed commentary on AMC in our company comment section, but the company is performing well after bedding down its major Bemis acquisition, notwithstanding input cost pressures.

Orica, the industrial explosives producer, has come through a difficult year as important sections of its customer base were disrupted by COVID-19 shutdowns and restrictions. The company has also been dealing with rectification work on one of its major ammonium nitrate plants, its Burrup facility in WA. Positively for the company, the COVID-19 disruptions have eased and management indicate its Burrup plant is now performing well.

Orica’s outlook for 2022 is looking more positive than it has for some time as production of commodities globally is anticipated to continue growing as economies and industrial production lift, along with pricing discipline broadly mitigating any input price pressures.

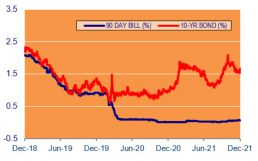

Interest Rates

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: IRESS

It appears that the final quarter of 2021 has witnessed the turning point in the interest rate cycle worldwide. Interestingly, the New Zealand Reserve Bank was one of the first central banks to raise its official cash rate doing so at both its October and November meetings by 0.25% to now stand at 0.75%. The decision was based on its medium-term outlook for inflation and employment.

The Bank of England Monetary Policy Committee (MPC), increased the Bank rate by 0.15% to 0.25% at its December meeting, citing the fact that inflation appears likely to exceed its targets until the second half of 2022.

In Australia the Reserve Bank (RBA) considers that the current up tick in inflation is only transitory, maintaining the cash rate at 0.10% and continuing to purchase government securities at the rate of $4billion a week until at least mid-February 2022. The RBA has been emphatic that it will not raise the cash rate until actual inflation is substantially within its target range.

Finally, in the US the Federal Reserve is concerned about the prospects of higher inflation and is tentatively forecasting three rate hikes in 2022.

In summary with Central Banks worldwide raising interest rates we believe it will be difficult for the RBA not to raise the cash rate during 2022.

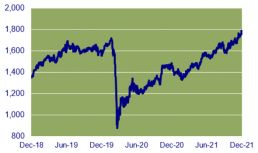

Property (REITS)

ASX Property Graph

Source: IRESS

It was a very strong quarter for the A-REIT sector, with the index returning 10% for the quarter, outperforming the broader All Ordinaries Accumulation index.

Despite concerns over rising inflation and bond yields, demand for investment in income generating assets (like real estate) remains strong, driving asset values for most property types. The key beneficiaries from this are real estate fund managers like Charter Hall, Home Consortium, and Centuria Capital Group. During the quarter, Charter Hall twice upgraded its earnings guidance for FY22, driven by valuation uplift and performance fees.

Also, during the quarter, Home Consortium’s listed vehicle, HomeCo Daily Needs REIT (HDN), announced a merger with Aventus (AVN). The potential merged group will be managed by Home Consortium, substantially increasing Asset Under Management. As for HDN and AVN shareholders, the merger will be earnings accretive and substantially increase the landbank for future development.

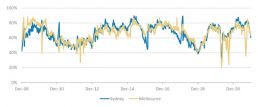

As for residential property, there has been a lot of focus towards the end of the quarter on a supposedly weakening residential market, led by auction clearance rates having fallen to around 60% in the two biggest markets, Sydney, and Melbourne. However, although clearance rates show some moderation, volume-wise both cities are still showing very strong numbers. This highlights demand for residential properties remains very robust, which should continue to provide a strong backdrop for developers like Mirvac Group and Stockland.

Resi auction clearance rate – weekly, since 2008

Source: CoreLogic, Morgan Stanley Research

Estimated successful sales (transactions) via auctions, since 2008

Source: CoreLogic, Morgan Stanley Research

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright 2021 Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst