As at December 2022

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

In the September quarter Market Commentary, we observed that the increases in interest rates commencing in August 2021 had had a marked effect on asset valuations. The bifurcation of the market into “growth stocks” and “the others” ceased to be as marked in terms of valuations, as had been the case for the previous four or five years (that is, the extraordinarily high prices for growth stocks and the low prices for more mature companies has become far less pronounced).

Dow Jones Industrial Average v NASDAQ

Source: Capital IQ

As an illustration of how these two groups of stocks have moved since interest rates started rising, the chart below shows the relative movement of the Dow Jones Index, the home of mature companies, against the Nasdaq, which comprises mostly of growth companies. From the high, at the beginning of November 2021, the Nasdaq fell 33% compared to the Dow Jones which only fell 8%. In the last quarter the divergence was particularly marked with the Nasdaq falling 1%, but the Dow Jones rising 15%. This illustrates the powerful tendencies of markets to revert to the mean (or long-term averages) valuation metrics. Other examples of this tendency occurred in the late 1960s (the Nifty Fifty stocks) and in the aftermath of the 2000 the tech bubble.

We would also like to re-iterate comments made in September that there are now a lot of companies that have returned to prices which make their long-term operating returns attractive. We feel that this is the key factor in making investment decisions, whereas predictions of short-term economic growth and suchlike require such a large margin for error as to make them useless in an investment sense.

As is discussed below there is a far greater range of stocks that we feel are attractive from an investment point of view in both the global and domestic markets. These range from the large tech sector companies where the returns on capital are very high (this attractive characteristic had previously been negated by excessively high share prices) to companies such as James Hardie, Harvey Norman and JB HiFi which have dominant positions in mature markets. We also retain our positive view of sectors where there is not high growth, but where there are very solid operating returns. Examples are in healthcare, banks, and insurance companies.

International Equities – Hugh MacNally

International Equities Performance

Source: MSCI

After falling 18.1% over 2022 the MSCI, a global index of stocks, rose 9.8% in the last quarter.

As was commented above, the rise in interest rates put pressure on the valuation of excessively valued growth stocks globally, while leaving those with more modest valuations only modestly down. The valuation of the stocks in the portfolios we think are attractive; this has been the case for some time for the stocks in mature industries. However, growth stocks, where revenue growth is high and high rates of return on capital are also high, have only recently become attractive. We started to build up positions in the portfolios in the latter group during the last two quarters. We would anticipate continuing this in the coming quarters and are looking for further candidates that are at an earlier stage of development to the behemoths (but have high rates of return on capital and can be acquired at an attractive price).

We are taking the opportunity during this period to review holdings we have bought over the last few years. In the food sector we are becoming a little less enthusiastic about the longer-term outlook. While the managements of both companies we hold have made useful improvements to operations and have refreshed the portfolio of products we are concerned that adequate returns are not being generated.

- Kraft Heinz was bought very cheaply after the acquisition of Kraft. The new CEO has restored order to the company but has not been able to generate the returns on capital that would be required of a longer-term holding. This is not a disastrous situation rather one where we are just doubtful whether the required return for investors can be achieved.

- Nestle, in a similar way, has restored the sales growth to respectable levels and improved the margins, but has done this via acquisitions which have required too much capital to be employed and as a result have not generated the returns we had hoped for. Again, not a situation where we feel concerned about the operations, rather it is the lack of adequate return.

We are quite happy with the insurance sector operating performance. Allianz dealt quickly with an embarrassing investment fund issue that had a severe but temporary impact on the stock price. At the current price, the underlying return we think is quite attractive. Travelers’ Companies, a US insurance company, has been performing well, however the price of the company is now extremely high. At over twice book value it is going to struggle to deliver a high enough return to justify the price. Our view is that a sustainable 15% return on capital is about as high as Travelers’ can expect in a mature market like the US. We think that it may exceed this for short periods of time but would not rely on higher rates of returns in the longer term.

We remain comfortable with our banking investments Lloyds and Wells Fargo, which are benefitting from higher interest rates (bank margins tend to improve with higher rates) and feel that the loan books are very conservative and should be resilient in a modest recession. The banks have a lot of capital and are in a vastly different situation to that of 15 years ago prior to the GFC.

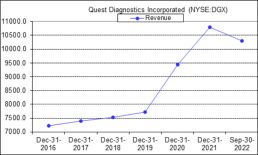

In the healthcare exposures, such as Merck Inc, Universal Health Services and Quest Diagnostics (we have commented on the first two recently), the latter is a provider a pathology services in the US and is one of two dominant providers. In contrast to its normal consistent rate of revenue growth Covid resulted in a large jump from the processing of tests, as can be seen on the chart below. As revenue returned to more normal levels of growth the share price fell sharply. This provided an opportunity to acquire stock at very attractive prices. The company has successfully pursued an industry rollup strategy for many years and continues to do so. Acquisitions are in the $10-100 million range. The company has produced a return of about 11% p.a. for shareholders over the last 10 years and we think that the business can deliver repeatable returns for the future. The company delivered a steady growth in earnings during the difficult economic times in the GFC, with earnings in the 5 years after 2007 doubling.

Quest Diagnostics Sales 2016-22 (US$Mill.)

Source: PPM and Capital IQ

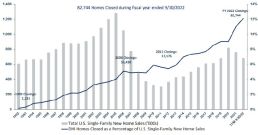

It might seem controversial after the doubling in mortgage rates in the US to be positive in the outlook for a residential home builder. DR Horton is the largest single family home builder in the US. Despite the boom in house prices there has not been a boom in construction levels, which have been modest by historical standards – this has been a very different boom to the one that eventually fed the economic crisis of 15 years ago. The chart below shows the number of homes constructed in the last 12 months was approximately 600,000 which is half the peak level and below the average over the last 30 years.

US Single Family Homes Construction 1992-2022

Source: DR Horton Q4 2022 Report

One sector of the market that has not returned to more normal valuations is luxury goods. There are a number of companies we like from an operational point of view but are not attractively priced in our view. These include the French luxury goods houses LVMH, Hermes and Ferrari.

Australian Equities – Peter Reed

Australian Equities Performance

Source: Capital IQ

The Australian equity market commenced the quarter not far off its year low of 6,600, before staging a rally as expectations for further official interest rate hikes moderated. At this point the market appears to be expecting two further rate hikes early next year before pausing for this cycle.

Banks were prominent in earnings releases with ANZ, NAB and WBC announcing FY22 results. Notable was a lift in net interest margins. Higher margins were particularly evident toward the latter part of the fourth quarter, indicating strong momentum going into FY23. For example, NAB’s average margin rose 4 basis points to 1.67% with the so-called exit margin lifting a further 5 points to 1.72% and with prospects of further strength for the ensuing 6 months.

A rising rate environment is generally positive for bank margins as the rates on the loan books tend to rise at a faster pace than rates on the deposit base. We do note, however, that as expectations moderate for further hikes by the RBA the banks are tempering margin guidance through second half FY23.

Bank lending growth has been generally healthy (+7%) as business lending growth offset a slowdown in mortgage loan growth. Further, loan book quality remains healthy on the back of low bad and doubtful debts. We will continue to monitor this situation closely as higher rates increase the risk of mortgage stress, which should become more apparent by mid-year as 2-year fixed mortgages roll off low rates to much higher levels. From a valuation view we are broadly neutral toward the sector, favouring the relatively cheaper stocks of ANZ and WBC.

Elders, a rural supplies company, has been a long-held position in PPM portfolios. Recent share price performance has been weak with the stock trading below $10, against a high of over $14. Despite the price performance the underlying business, on our assessment, continues to perform well as the company benefits from strong agricultural commodity prices and favourable climatic conditions, despite some regions being affected by floods. Our view is that through-the-cycle earnings place the company on attractive valuations, which was the case prior to the share pullback and is even more the case post the pullback. We believe the company remains capable of delivering mid-teen levels of return to the equity investor; in its FY22 results the company delivered a 26.2% return on capital, well above its hurdle rate of 15%.

Macquarie Group delivered another solid performance with its 1H FY23 results. Overall profit was up 13% year on year, producing a 15.6% return on equity. Besides its capital markets focused business, which suffered from lower activity levels, each of the banks’ other businesses delivered solid rates of growth.

Macquarie Asset Management (MAM) saw net profit gain 28%. We see this business as well placed to leverage off the massive spend required to transition the world energy markets from one chiefly reliant on fossil fuels to a zero emission, renewables-based market. Globally, the investment spend will total in the hundreds of billions of dollars over decades, which plays into the Macquarie’s extensive global network.

The other two business groups, BFS (Banking & Financial Services) and CGM (Commodities & Global Markets), delivered similarly strong performance with profits up 20% and 15% respectively.

Our view on MQG is tempered by its market valuation greater than 2X book value, delivering an underlying return profile of less than 10% pa. For the time being we will continue to monitor the position through the lens of the energy transition and prospects that the company will “grow into” its valuation.

We would re-iterate the comments made in September about out of favour industries where the prices of some high-quality companies have been pushed down to levels where the underlying returns seem very attractive. In particular, the portfolios have tended to add to holdings in JB HiFi, Harvey Norman, and James Hardie. The latter, having more than halved in price, has returned to attractive levels. We retain a favourable view of the main market, US residential construction, where construction levels have been modest compared to demand for many years.

We continue to look at opportunities in the energy market, where we can earn an attractive return. The irrational approach of governments of all leanings has created disruptions and price spikes in numerous areas. Price caps and controls in areas where increased production is vital are unlikely to produce the intended result. We will look for opportunities where we can earn a high rate of return; we think these opportunities will materialise in due course.

Interest Rates – Ian Hardy

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

2022 has witnessed the steepest rise in interest rates for many decades as central banks around the world attempt to reduce inflationary pressures. The last quarter has seen continued rate rises and in late December the Bank of Japan widened the band within which it allows the 10-year bond yield to trade from 0.25% to 0.50%. Whether this leads to higher or even positive short-term yields in Japan is yet to be seen.

At its last meeting for the year the Federal Open Market Committee (FOMC) increased the Federal Funds target by 0.50% to a range of 4-1/4 to 4-1/2% as US inflation remains well above target of 2% over the longer run. The commentary accompanying the rate rise suggested further rate rises, with the market predicting a terminal rate of 5.1% in 2023. Once again, the Committee confirmed that it will continue reducing its holdings of Treasury securities and other similar assets.

The Bank of England Monetary Policy Committee (MPC) also increased rates in December, raising the Bank Rate by 0.5% to 3.5% and noted that “the labour market remains tight and there is evidence of inflationary pressures in domestic prices and wages that could indicate greater persistence and thus justifies a further forceful monetary response and further increases in the Bank Rate may be required for a sustainable return of inflation to target.”

In Australia, the Reserve Bank (RBA) continued to raise rates over the quarter and at year end the cash rate was 3.10%. The Board noted that it expects to increase rates further over the period ahead but subject to incoming data and the assessment of the outlook for inflation and the labour market. It is interesting that the RBA has been less aggressive with its rate rises than other central banks, which suggests that it will tread very carefully in 2023 to avoid a recession in Australia.

Property (REITS) – Franklin Djohan

ASX Property Graph

Source: Capital IQ

Despite rising 11.6% in the last quarter, the ASX Property Index nevertheless fell heavily over the year, falling 20.1% and significantly underperforming the broader All Ordinaries Index.

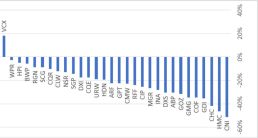

The sector has been one of the most impacted by the interest rate rises this year, both from the point of view of the underlying asset valuations and from the impact of higher interest payments for servicing debt. Property asset managers who have benefited most from the low interest rate environment, with hefty FUM (Funds Under Management) inflows and positive asset revaluations boosting top line growth through higher management fees and oversized performance fees, have seen their share prices grow strongly during the pandemic. However, these asset managers have given back all their share price gains as interest rates rose during 2022 and become the biggest laggards during the year. Examples of such underperformers include: Centuria Capital Group (CNI) down 51%; HMC Capital Ltd (HMC) down 46%, and; Charter Hall Group (CHC) down 41%.

In other sectors, industrial, property developers, and office REITs (Real Estate Investment Trusts) prices were down 15-to-35%. Retail tended to fare better and was down less than 10%, however, this was mostly because valuations were originally at low levels and share prices remained around or below pre-pandemic levels. There were exceptions, Vicinity Centres (VCX) ended up 18% for the year. The company owns large retail shopping centres, which were severely affected by Covid, but which have had improved operating conditions recently, as indicated by the latest results. However, the rise in share price only brings Vicinity back to the pre-pandemic level.

After a big correction in the listed property sector, a lot of the bad news we feel has been priced in by the market. Most of the listed operators are trading below their Net Tangible Assets (NTA). The focus should now be more on the operational results and trading conditions rather than valuations. Some opportunities may arise from the 2022 correction.

2022 Share Price Movement

Source: S&P Capital IQ, ASX

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst