As at June 2021

Equity Market Returns

Source: IRESS

Overview

Developed and emerging economies have recovered far more strongly than was expected 15 months ago as a result of massive fiscal and monetary stimulus. The growth for the 2021 calendar year is anticipated to be strongest in Asia with GDP growth of approximately 7.5%, the US 6.3% and Europe 4.1%. Australia’s growth is expected to be 5.0% after a contraction of 2.4% in 2020. Unemployment has also fallen sharply and there are labour shortages in certain areas. Shortages and price inflation have also appeared in commodities ranging from lumber to computer chips. The issue that is concerning the markets is whether the increase in inflation recently reported is temporary or is going to be ongoing.

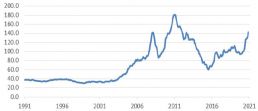

While some of these shortages are likely to be temporary resulting from supply chains re-starting, it is a development to be closely watched. As an indicator, the chart below shows the RBA commodity index over an extended period. Over the last year this index is up approximately 40% – while this is substantial, it is not dissimilar to the increase during the same period after the GFC in 2009. It might be remembered that similar inflation concerns arose after the GFC, with the same arguments being put forward as are now appearing. The result turned out to be benign that time, however, there is no guarantee that the current situation will have as benign a result. Given the crucial role of inflation on interest rates and in turn on asset valuations it is something to be watched closely.

RBA Commodity Index in US$

Source: RBA

Short term interest rates in developed economies have been kept at close to zero despite stronger than expected economic data. To date central banks have merely stated that they will bring forward plans to increase rates to a 2022-24 timeframe (some considerable time off). They have also continued the extra-ordinarily high levels of support for bond markets, although very recently have indicated some degree of tapering.

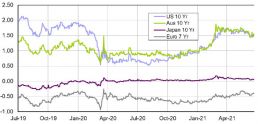

The above, although only modest indications of action, would have in the past caused a significant rise in bond yields (as occurred in 2013 and 2018). As can be seen from the chart below, which covers the last two years, bond yields have risen in the US (and in Australia) from the lows at the start of Covid-19 crisis, but not substantially, and remain at broadly similar levels to those prior to the crisis and in the last few weeks yields have actually fallen. These are somewhat contradictory developments. In Europe and in Japan yields remain close to zero or negative.

Government Bond Yields

Source: FRED

We have long expressed the view that the major market risk is the high levels of valuation of popular sectors such as technology, luxury goods or in Australian health care. Valuations are very high multiples (by historical standards) of revenue, earnings or capital and our view is that these valuations are vulnerable to adverse developments such as rising cash or bond yields.

We feel however that sectors of the market where this is not the case are less vulnerable. Examples are: the finance sector (banks and insurance), manufacturing, telecommunications and pharmaceuticals, where valuations are close to or below long-term averages.

There have been periods where there has been a divergence in valuations of companies similar to the present and in these cases the returns to investors have also varied widely when the speculative fervour ends – very much in favour of the attractively valued, which is where PPM portfolios are positioned.

We expect that there will be a recovery in dividends in the near term and that a number of companies will pay special dividends or have increased buy backs. The finance and resources sectors in particular have very high levels of capital (and less inclination to embark on adventures than in the past) and are in a position to pay large special dividends. A welcome change of behaviour for shareholders.

International Equities

International Equities Performance

Source: MSCI

The MSCI, a global stock index, was up 9.3% for the quarter and 27.5% for the latest 12 months. The A$, which recovered to the level it has traded for the bulk of the last five years, had only a minor effect on the return for the quarter (expressed in A$), but still had a large negative impact on the one-year return.

The recovery in undervalued sectors continued during the quarter, including: pharmaceuticals, banking, manufacturing, consumer staples and some technology.

While the market valuations in these sectors have improved substantially from the lows of fifteen months ago, they remain at the lower end of long-term averages. Operating returns have generally improved but are not at levels that would cause concern of being overheated, with the possible exception of residential construction.

In the pharmaceutical sector there was a broad improvement in values. Stocks with large oncology franchises such as Merck and Bristol Myers have continued to experience rapid growth in sales. In this area Merck’s sales reached an annual $19 billion which is significant for a franchise that barely existed six years ago. The best returns however were in the diabetes drug producers, Eli Lilly and Novo Nordisk. In the case of Lilly there was also encouraging news for their Alzheimer’s drug candidate. During the quarter there was regulatory success for another Alzheimer’s drug which increased the market’s interest in this treatment area. This approval was significant, because the area has been a graveyard for research ever since the identification of the condition. However, the regulatory approval was controversially in that it was given against the advice of the relevant FDA scientific advisory committee. Nevertheless, Lilly’s candidate benefitted by association. The area appears to be receiving favourable regulatory treatment given the immense and rising cost the disease is inflicting on health systems.

Bank valuations improved strongly post the March quarter reports, which showed continuing improvement in operating conditions. Banks are holding substantial excess capital and with the recent passing of regulatory stress test, the likelihood of large dividends and buybacks would appear to have improved. Asset growth has increased above the anaemic levels of the last few years, which bodes well for the longer term. An additionally positive trend among commercial banks is the simplification and rationalisation of their businesses, which we feel will result in better use of capital, the returns from which are improving but are still well below historical levels. The two stocks we hold remain substantially undervalued in our view.

The consumer staples stocks we hold also rose strongly after the quarterly results (for Kraft Heinz). Operating performance improved substantially in both sales and margins. Kraft Heinz share price has retreated very recently as concerns arose about their cost inflation not being able to be passed on. This we believe will be at worst temporary and is related to agricultural input prices, particularly grain prices. The more important aspect is the improvement in operating efficiency and the refocussing of their product portfolio, which we think has a long way to go.

We have acquired a position in the US hospital operator Universal Health Services (covered in more detail in the quarterly report stock comments). The company operates acute care hospitals, behavioural facilities and surgical centres across the US and in the UK. It has had a long history of consistent returns and is priced very attractively.

Possibly the most disappointing sector to date is telecoms. While the industry structure is now more attractive, the participants have yet to extract better margins from their mobile operations (in contrast to the situation in Australia). An improvement in pricing and margins is a key component of our investment case. We will be looking to see that this starts to occur; in the past it has been triggered by the changeover to the next generation of mobile technology (in this case 5G), which is presently at an early stage.

We retain, at reduced exposures, holdings in Microsoft and Google – these are both great companies, but the pricing of the stocks has been for some time far too high. We would look to enter or re-build the positions if there was an opportunity to do so at an attractive price.

Australian Equities

Australian Equities Performance

Source: IRESS

Although there may be some questions about valuations of certain sectors of the market, it is interesting to note that the index has only now moved decisively above the previous all-time high recorded prior to the GFC in November 2007. In other words, it has taken 14 years for it to regain its previous level.

The major Australian miners in the portfolio, BHP and Rio, were little changed over the quarter. However, the stocks are trading comfortably above their pre-covid levels as well as the previous peaks during the resources boom circa 2008/ 2009. Given the cyclicality of the sector and the unsustainably high price for iron ore we are cautious, however it might be noted that the market has already assumed a much lower long-term iron ore price and both companies are distributing their massive cash flows to shareholders (rather than buying highly priced competitors as they have tended to do in the past). There appears to be a strong argument that strength in the sector may be longer lasting.

We note that many commodity prices have been driven to record highs, in part on the back of surging Chinese demand, but we also note that this demand is likely to be joined by additional demand from other major economies as they emerge from the covid downturn. The US administration has recently announced a $1.2 trillion infrastructure plan, which would see a big boost in spending on roads, bridges and the like, all of which require large volumes of raw materials. Other major economies have similar plans under way.

At the same time supply of many of the key raw materials are constrained. Unlike the last mining boom, when the miners sharply increased capex in order to boost production, for some time now they have demonstrated a high level of discipline when considering capital expenditure plans. The oft-stated mantra of value over volume has been pushed particularly by the Australian iron ore producers. This is basic economic sense since a modest $10 rise in the price of iron ore is much more valuable to the miners than a significant increase in volume of, say, 100 million tons. (Australia currently produces a little over 900 million tons of iron ore per annum.)

Compounding this position is a heightened demand outlook globally for commodities associated with the transition towards renewable energy forms and the reconfiguration of the energy and transport sectors. This involves everything from copper and steel – intensive wind turbines to batteries with their resultant demand for graphite, nickel, copper, lithium, cobalt, among others. In short, the environment for higher-for-longer commodity pricing appears positive.

Further, the strength of the major miners’ balance sheets, with modest debt levels, implies the outlook for returns to shareholders in the form of dividends and share buybacks is strong.

Performance of the banking sector remains positive. We have maintained a strong weighting in the major trading banks on the basis of healthy loan books, strong capital levels and improving returns on equity. It is often the case that difficult conditions allow the dominant companies in an industry to enhance their dominance. This was the case during the GFC and is again the case this time around where the position of the top 4 banks has strengthened.

The banks are benefitting from a pickup in housing credit growth with strong growth from owner occupiers as well as increased borrowing from investors. Rather than worrying about a fall in housing prices, which was the case early in the covid downturn, the anxiety now, at least from the RBA, is the level of house borrowing and ensuring the banks maintain appropriate lending standards. We remain buyers of the banking sector.

Corporate activity, including spin offs and mergers and acquisitions, has been a feature of the market, induced by a strong recovery in the market from its covid lows as well as historically low interest rates. The spin off by Woolworths of its Endeavour drinks business is an example of this as well as the recent takeover bid by a group of superannuation funds for Sydney Airport. We would expect heightened M&A activity to continue and to be a support for the overall market.

A further feature of this period has been a build-up of price pressures in certain segments of the economy. Notable has been the construction industry where strong demand for housing has met with supply constraints partly, but not always, as a result of Covid issues. The RBA appears confident at this point that the price pressures are mainly transitory and will normalise as economies themselves normalise. However, this will bear close monitoring as the degree of stimulus applied by the government here as well as overseas is historically significant. Partly for this reason we believe some exposure to inflation hedges, such as gold producers, is appropriate.

Interest Rates

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: IRESS

The Reserve Bank of Australia (RBA) kept the cash rate at 10 basis points (0.10%) and has stated it will not increase the rate until inflation is sustained in the 2 to 3 per cent target range for some period of time. “The Bank’s central scenario for the economy is that this will not be met before 2024. Meeting it will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently.”

In keeping with the cash rate at ten basis points, the RBA is retaining the April 2024 Commonwealth Bond as the bond for the yield target and keeping the target at 10 basis points. The Bank will continue purchasing these bonds at $5 billion a week until early September and then at $4 billion a week until at least mid-November.

The aim of these measures is to provide the monetary support that the RBA believes the economy requires as it transitions from the recovery phase to the expansion phase as the economy emerges from the impact of the Covid-19 virus.

In the US, the Federal Reserve has kept the Federal Funds rate and the pace of asset purchases unchanged and like the RBA has noted that this will continue until “substantial further progress has been made“ in employment and inflation. The prospect is for rate rises to occur in the US by the end of 2023.

Finally, it is worth noting that the 10 year Australian Government Bond rate is 1.49% and the equivalent rate in the US is 1.35%.

Property (REITS)

It was a strong quarter for the listed property sector, up 10.7%, outperforming the broader All Ordinaries index.

With over a year since the Pandemic hit, we saw the change of preference towards freestanding homes. The amount of government stimulus and the low interest rate environment has only added fuel to the residential housing market. This has benefited residential developers Stockland and Mirvac.

The growth in demand for industrial property remains strong, and the pandemic has accelerated online retail which is one of the key drivers for this growth. It is no surprise that more money has been put into the industrial property sector, with both listed and unlisted players continuing to diversify into this growing sub-sector.

ASX Property Graph

Source: IRESS

Goodman Group, the largest listed industrial property player has been the beneficiary of this trend. Goodman’s share price outperformed the broader property index, up almost 17% for the quarter. Similarly, the Centuria Industrial REIT also outperformed, up 12% for the quarter.

The office sector property players continued their share price recovery as well. Dexus’ share price increased by 9% during the quarter. It is now trading roughly in-line with its Net Tangible Assets (NTA). However, uncertainty remains about the future of office space with the structural headwind coming from the “working from home” trend.

Another trend that appeared during the Pandemic was an increased preference to shop in local neighbourhood shopping centres. This trend has certainly benefited our investment in Home Consortium, which develops and manages these types of shopping centres. Low exposure to the type of discretionary spending that is being disrupted by online shopping was also positive. Home Consortium was up strongly during the quarter (up 23.6%) and its recent spinoff, HomeCo Daily Needs, which owns the centres, was up 10.2%. This contrasts with centres with high discretionary retail exposure such as Vicinity Centres and Scentre Group, which are both trading at a big discount to their Net Tangible Assets.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Senior Client Relationship Manager with any questions, comments or suggested improvements at jm@ppmfunds.com or phone her on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright 2021 Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst