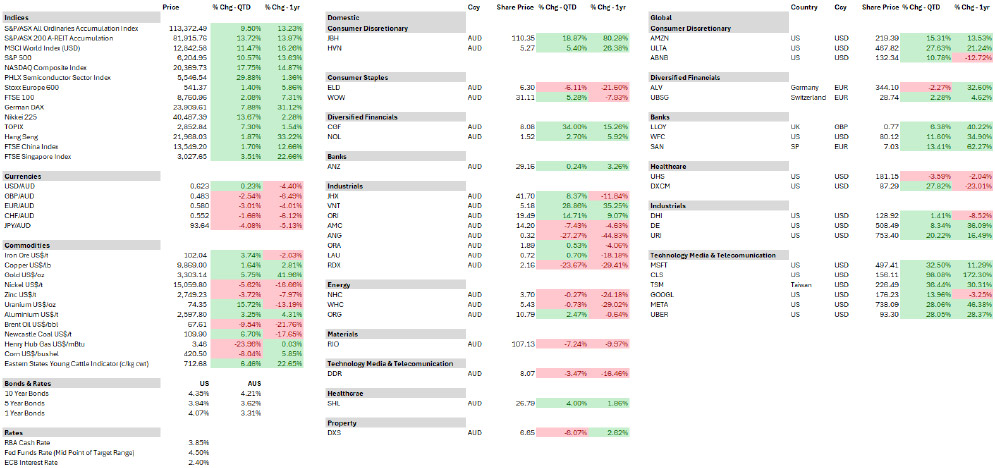

As at June 2025

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

The financial year ended with strong gains in global markets and gains in the domestic market.

However, at the beginning of June quarter, markets suffered a rapid decline after the announcements by US President Trump of an aggressive tariff plan. The episode lasted approximately one month, by which time the global markets had returned to where they were. It is interesting to note that those on whom the tariffs were to be imposed suffered less than the US. There seems, at this point, to be no clear pattern or strategy to what is a confusing amalgamation of deals and threats.

Global equity markets recorded a positive year, with the MSCI All-Country World Index rising 18.5% over the past twelve months and 6% in the most recent quarter (in A$). Among developed markets, Germany led with a 29% increase, while Europe as a whole and the UK each returned around 10–11%. In the United States, technology stocks contributed to selective high returns—though the Nasdaq Composite only advanced 15.4% —with Microsoft (+7.4%), Amazon (+11.3%) and Google (–3.6%) marking more subdued performances amid ongoing debate over AI-related spending. In Australia, the All Ordinaries Accumulation Index ended + 13.2% for the year and + 9.5% for the quarter, supported by information technology, financials and communications; detractors to that trend included materials, utilities and healthcare.

Globally, banks saw improvements in return on capital, which in many instances approach or exceed 15%, while valuations appear attractive. European banks recorded notable share-price gains—Lloyds was up 39% and Banco Santander 68%—and Wells Fargo in the U.S. rose 39%. In Australia, ANZ reported 5% revenue growth in its half-year to 31 March 2025, although net interest margins fell. Given the elevated valuation multiples of domestic banks, exposure to European and U.S. counterparts are preferred.

Monetary policy continues to favour a cautious approach and steady short-term rates for the present. The Reserve Bank of Australia maintained its cash rate at 3.85% in July—following a 25-basis-point cut in May—citing a balanced inflation outlook (core inflation at 2.9%). Ten-year Australian government bond yields moved up to 4.36%, reflecting expectations of a cautious, data-driven approach to further easing. In the U.S., the Federal Reserve is likely to hold rates steady in July, with the ten-year Treasury yield at about 4.41% amid projections for cuts later in the year. The European Central Bank trimmed rates by 25 basis points in June, while the Bank of England left its base rate at 4.25%, with markets pricing in an August reduction as economic growth moderates.

The property sector delivered a return of 13.97% for the 2025 financial year, largely driven by a 13.72% gain in the final quarter. Retail property trusts such as Vicinity Centres and Scentre Group closed the gap on net tangible asset values, supported by ongoing consumer spending and constrained new supply due to high construction costs. Office markets diverged across cities: Sydney and Brisbane saw rising face rents and reduced incentives, whereas Melbourne continued to face downward pressure on effective rents alongside higher incentives.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global Equities markets rose 18.5% over the last 12 months, as measured by the MSCI (a global stock index) in A$ and 6.0% for the last quarter. Despite the strong performance of a number of technology stocks, overall, the sector only rose 15.4% as measured by the Nasdaq Index. Among the developed markets the best performance was by the German market which rose 29%, while overall the European and the UK market rose a more modest 10-11%. The Chinese market rose strongly on the back of recovery in finance and tech sector stocks; the rises were particularly marked among the banks.

Globally, banks had a strong year and generally, they are attractively priced, and their operating performances have improved significantly. An important measure of this is the return generated on capital, which has been improving for some time and is now close to or above 15%. Share price returns for European banks were especially high, with Lloyds up 39% and Banco Santander, a large Spanish bank, up 68%. Wells Fargo, a long-held part of the global strategy was up 39%. Insurance stocks also rose strongly, the European insurer, which has been held in the portfolio for over 10 years, Allianz, rose 37%.

While the Nasdaq as a whole rose only 15.4%, there were some very high returns from individual stocks. In the portfolios, Celestica, a supplier of equipment and services to datacentres, rose 165%. The company is benefitting from the massive increase in demand for computing power. Others to rise strongly were: Uber up approximately 50% from the time we started buying it in late December 2024, Meta (up 40%), Taiwan Semiconductor (up 29%). The major tech stocks had restrained performance over the year; Microsoft (up 7.4%), Amazon (up 11.3%) and Google (down 3.6%). Concern over the emergence of massive capital expenditure plans and the unknown economics of the deployment of AI were contributing factors. During the year, the concerns abated and there were very much better performances particularly in the last quarter.

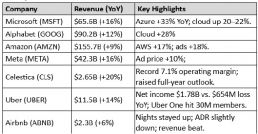

As can be seen from the table below, revenues continued to grow strongly for the sector particularly in the divisions related to cloud, which is not surprising. Of course, revenue growth is not the whole story – it is not sufficient, but it is necessary.

Q1 2025 Earnings Summary (Quarter Ended 31 March 2025)

Source: Company Results CY2025 Q1

Industrial sectors also did well, with the portfolio stock United Rentals rising 21.6%. United Rentals hires out plant and equipment to the construction and other industries. United is the largest in the sector, with growth coming in roughly equal parts from bolt on acquisitions and organically.

From December we started buying Uber Technologies based on the growth in revenues and rapidly increasing free cash flow (that is the amount of cash the company is generating after expenses and capital required for growth). As yet, we are unsure as to how the role of automated vehicles will evolve and whether this will be competition or a benefit for Uber. Our view is that this question will take some considerable time to be decided but, in the meantime, the price and growth of Uber revenues make it an extremely attractive proposition.

A similar revenue and free cash flow pattern has also emerged for Airbnb. Over the last 5 years (starting prior to Covid) revenues have grown at an average rate of 17% p.a., and free cash flows have gone from negative $95 million to $4.5 billion last year. There has been commentary about pushback in popular residential locations, such as in cities like Barcelona, but while newsworthy we think the growth numbers tell the more important story. We argue that these platforms are expensive to set up but once revenues reach critical mass the bottom line starts to grow by multiples. In the case of Airbnb, expenses grew 62% and revenues increased 131%.

We would observe that there has been a breadth in the range of industries that have performed well this year. It has not been confined to a small number of very large stocks. This has been in an environment of extraordinary swings in government policy, which affect an extraordinarily wide range of industries.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Bloomberg

The Australian equity market looked through early volatility and tariff concerns during the quarter to register solid returns: The All Ordinaries index gained almost 10% on an accumulation basis, led higher by information technology, financials and communications. Laggard sectors included materials, utilities (absolute declines) and healthcare. On an individual stock basis, Challenger, Ventia and JB HiFi led the gains among portfolio stocks while Rio, Amcor and Elders were among the detractors.

The bulk of the market will report FY25 results starting next month, but for the quarter just ended the main reporting activity centred around NAB, ANZ and Westpac’s first half earnings results (to 31 March 2025), which were broadly similar. PPM’s exposure is mainly through ANZ, as the cheapest bank in the sector; this is where we will focus our commentary. While banks are a major sector in the Australian market, our concern is that the pricing, and this is particularly the case for CBA, is unattractively high relative to their earnings capacity since the GFC and more recently the Royal Commission in 2018.

ANZ delivered revenue growth of 5% versus the previous half. The worrying factor is the decline in margins. The most important measure is the net interest margin (NIM), which is the difference between the bank’s borrowing and lending rate. For the half, ANZ saw its NIM decline 3 basis points (similar to its peers). The pressure is primarily funding related and indicates competition among the banks to attract deposits remains strong. With forecasts of cuts to the official interest rate, the banks will face headwinds in improving their NIM position given that a declining rate environment typically squeezes margins.

Despite this, the sector led by CBA and NAB, has significantly outperformed the broader market.

With valuation multiples expanding, we question the basis for this performance and prefer bank exposures in Europe and the US.

Orica, the industrial explosives manufacturer, reported earnings during the period. The company has long been well positioned to capitalise on an attractive industry structure where it will typically share a regional market with one other competitor. However, for some years this position has been hampered by operational difficulties at its key WA ammonia nitrate plant at Burrup. With the rectification work for this facility now behind it, the company is better positioned to benefit from still-buoyant market conditions.

Results for the half year to 31 March saw earnings rising 34% against the previous corresponding period, handily outperforming market expectations as the company’s core blasting solutions business performed strongly. Results were rounded out with strong operating cash flow and with a dividend which was meaningfully ahead of market expectations.

We have re-established a position in Woolworths, having exited in early 2024 as political pressure built for an inquiry into the sector over cost-of-living concerns. In the ensuing period we have seen a further drop in share price as well as a handover of the management baton to new CEO. We view both developments as positive for the investment case.

For CEO Amanda Bardwell, we view the opportunity for refreshed management positively, and look for moves to wind back some of the ventures previously undertaken, bringing the company back closer to its core food and grocery operation. Exiting peripheral businesses, such as the recent decision to shut down its MyDeal online marketplace, is a step in the right direction and should ultimately lead to a higher return on capital. The biggest opportunity lies with fixing BigW, but legacy lease arrangements pose difficulties.

We note the underperformance in the portfolio of a number of stocks which we broadly categorise as distributors. These include agricultural company Elders, transport and logistics company Lindsay, Redox (chemical and ingredients distribution) and Dicker Data (IT equipment distributor). However, our view is that each company has a strong position in their respective sector and valuations are attractive.

The recent developments at James Hardie are very disappointing. We have thought that the company’s US business is very attractive, and we have been a shareholder for over 20 years. The extraordinary price the company paid to acquire another US building products company has changed the earlier held view dramatically. We are looking for an opportunity to exit the company. Together with the acquisition price, the approval, or rather lack of approval process, raises governance issues.

Interest Rates

Neil Sahai

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Bloomberg

The Reserve Bank of Australia (RBA) held the cash rate steady at 3.85% in July, following a 0.25% cut in May. While markets had anticipated another reduction, the RBA opted to pause, citing a more balanced inflation outlook and resilience in the labour market. The decision was split (6–3), highlighting internal debate over the appropriate pace of monetary easing.

Core inflation has eased to 2.9%, within the RBA’s target band, but GDP growth has slowed to 1.3%, and soft retail trade data points to weak consumer sentiment. A further rate cut remains possible in August, contingent on upcoming inflation data.

Australian bond yields rose in response to the RBA’s cautious stance. The 10-year bond yield climbed to approximately 4.36%, the highest since May, reflecting expectations that any further easing will be gradual and data-dependent. The upward-sloping yield curve suggests investor confidence in long-term economic growth.

In the U.S., the Federal Reserve is expected to hold rates steady in July but may adopt a more dovish tone if inflation slows or the labour market softens. Despite renewed political pressure for cuts, the Fed remains focused on price stability and full employment. The 10-year Treasury yield has eased to around 4.41%, reflecting growing expectations of rate cuts later this year. Strong jobs data and easing geopolitical tensions have supported demand, though fiscal developments and tariff risks could influence inflation expectations.

In Europe, the European Central Bank (ECB) cut rates by 25 basis points in June, reflecting increased confidence that inflation is steadily returning toward target.

Meanwhile, the Bank of England (BoE) held its base rate at 4.25% in June, with inflation still elevated at 3.4%. A rate cut is widely expected at the BoE’s August meeting, as economic momentum continues to slow.

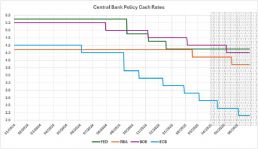

This chart summarises the cash rate paths of major central banks from early 2024 to mid-2025.

Central Bank Policy Cash Rates

Source: Bloomberg

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Bloomberg

The property index delivered a strong return of 13.97% for the financial year, with the vast majority of gains driven by a sharp rebound in the final quarter, which alone returned 13.72%.

The retail property sector delivered a strong performance over the past financial year, with Vicinity Centres (VCX) and Scentre Group (SCG) both posting solid gains, contributing to a narrowing gap between their share prices and Net Tangible Assets (NTA). Sector fundamentals remain robust, supported by continued, though moderating, growth in consumer spending, underpinned by strong population growth. Supply-side constraints continue to support the retail property market. New retail space remains limited, with development activity hindered by elevated construction costs and site availability. New supply is mostly concentrated in neighbourhood and sub-regional centres.

Office market conditions remain mixed across major cities. Sydney and Brisbane have seen a decline in incentives, while face rents continue to rise, indicating improving momentum. In contrast, the Melbourne office market remains under pressure, with incentives increasing and effective rents continuing to fall. Prime-grade assets are still outperforming lower-quality stock, reflecting the ongoing preference for high-quality space. Capital values have started to edge higher, supported by easing interest rates and stable cap rates. Dexus (DXS) recently revised its office portfolio valuation slightly upwards. While the headline increase was modest, it was driven by rental growth rather than cap rate compression, a positive sign of underlying demand.

Residential developers Stockland (SGP) and Mirvac (MGR) have also delivered strong performance, with a positive outlook ahead. This is underpinned by easing construction constraints, lower interest rates, and ongoing support from first home buyer incentives. Slowing growth in construction costs also presents margin upside for developers. However, growing affordability pressures may weigh on demand.

Stabilising construction costs and a recovery in regional property prices have also supported growth in the land lease sector. This segment continues to gain popularity, with key players including Ingenia (INA) and Lifestyle Communities (LIC). Stockland and Mirvac are also expanding their presence in this space. Meanwhile, GemLife started the process of raising $750 million through an Initial Public Offering (IPO). Once listed, it is expected to become one of the largest pure-play land lease community operators on the ASX.

Demand for industrial properties remains strong, particularly for high-quality, well-located assets. Rents continue to rise, led by Brisbane and Melbourne. However, incentives have also edged higher amid an uptick in new supply, a trend worth monitoring closely.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relations with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager