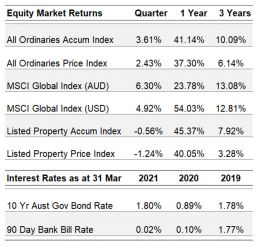

As at March 2021

Equity Market Returns

Source: IRESS

Overview

As can be seen from the tables above equities markets rose strongly from the lows of the Covid-19 collapse 12 months ago. The Australian equity market was up 41% and the global markets (in A$) up 24% for the year. The returns of global markets were muted by the recovery of the A$, which after falling sharply during the early part of the crisis to recovered quickly to more normal levels by the end of 2020, in effect reducing global returns by approximately 30% for the year.

In saying that the A$ has recovered to more normal levels, it has been in the range 65 – 80c for 75% of the last 35 years. Within this range there has been no discernible trend, merely fluctuations typically downward during economic crises and up to 100c in (commodity) booms, then a return to the range.

During the quarter, the Australian equities market was up 3.6% and the global markets up 6.3%. As is discussed later in this report the composition of market returns has changed significantly over the last six months. A greater contribution has been seen from “value” stocks*, particularly in the finance, manufacturing and consumer goods sectors. This development has been beneficial to the portfolios.

We remain very comfortable with the valuation of stocks in these sectors, but equally uncomfortable with the valuation of the market ‘darlings’, which while they might have come through the crisis intact, have valuations that are unsustainable – if history is any guide.

The company results reported during the quarter indicated rapidly recovering returns for many industries across the developed economies. Of particular note, has been the housing industry in the markets where the portfolios are invested, that is in the US and Australia. This outcome is in stark contrast to bank expectations 12 months ago and underlines the precautionary nature of their provisioning. Given that outcome, we think that they will continue to write back these provisions (the US banks have already started to do so). As a result, we would expect the sector will return to paying high dividends again. Additionally, they will also have excess capital which would be available to return to shareholders when Regulators allow.

The property sector, outside housing, has also staged a recovery, despite the concerns that have been expressed about changes to shopping and work patterns that developed during the Covid-19 crisis becoming more permanent. There is insufficient data yet to determine how much of the change is permanent and how much will return to previous patterns.

Cash rates have remained stable during the quarter with Central Banks reiterating their intention to keep rates at the current low levels for the foreseeable future. Longer term rates, however, continued to rise during the quarter, but remain at extremely low levels historically. In the developed economies they are either close to zero or negative in real terms. This obviously makes bonds extremely unattractive, for the long-term investor. While little inflation has appeared as yet, the amount of fiscal and monetary stimulus makes it likely that the beast from the 1970s will eventually re-awaken to feed on the unfortunate bondholder.

*Value stock are often defined as those where the current earnings, or returns, make them attractive investments, without the need to make assumptions about high future growth rates. Our view is that growth rates are mostly overestimated, often by a wide margin, and nearly always over-valued.

International Equities

International Equities Performance

Source: MSCI

The quarter saw a recovery in a range of industry sectors that had been ignored by the market for a number of years. It is difficult to point to any specific reasons why there has been a change in attitude, although the rise in long term interest rates over the last 9 months may have let a little air out of the momentum bubble. While prices of value stocks have risen sharply (in the case of the banks it has been in excess of 80%) we think that the stocks portfolios are invested in remain undervalued as they were so heavily discounted in the first place. A return of economies to more normal levels of growth we think will help alleviate this valuation discount.

There has been a marked recovery in demand in big ticket consumer items such as autos. This has benefited the components suppliers, such as Lear Corporation, which manufactures car seats (with approximately 25% global share) and wiring systems. It has also benefited manufacturers such as VW. VW is rapidly transforming itself in a major supplier of battery electric vehicles and is expected to overtake Tesla in volume of production in the near future. Unlike the new entrants, the valuation is attractive based on current earnings (as opposed to distant projections). VW owns a large range of brands from Porsche to Bentley and Audi to the more common Golf.

A sector that has remained relatively static over the last two years, despite revolutionary advances, is pharmaceuticals. Various short-term factors could be put forward for the negative sentiment, related to the Covid-19 lockdowns, but we feel the advances that have been achieved in oncology (the two main areas of treatment we have invested in are oncology and diabetes) warrant a much higher valuation. In the case of Merck, developer of the blockbuster drug Keytruda, anxiety has arisen over patents that expire in 7-8 years. This we feel is overly pessimistic given the rapid development of treatments in the area and Merck’s leading position – the concerns are in stark contrast to the unbridled optimism over the sometimes marginal useful developments coming out of other technology, in say, Silicon Valley!

We have discussed on numerous occasions the finance sector and our view has not changed regarding the attractiveness of the valuations. Although the financial strength of banks is now being accepted there are two factors yet to play out with the banks we hold. For Lloyds, it is the return to high dividend payments and for Wells Fargo it is the removal of the asset cap that was imposed three years ago, together with the reduction in its bloated cost structure. The recent price rises still leave these two banks at significant discounts to more normal bank valuation metrics. The same applies to the insurance sector (but to a slightly lesser degree).

While much of the tech sector is overvalued, we are looking for opportunities where this might not be the case. We have retained the investments in Cisco Systems and are looking in areas relating more to industrial applications as opposed to what might be characterised as “consumer” – advertising, consumer products, entertainment where much of the overvaluation occurs.

We continue to see improvements in operating performance of the holdings in the consumer products companies, Kraft Heinz and Nestle. There would appear significant room for further improvement, particularly in the case of Kraft, where the process of rebuilding markets and repositioning their portfolio of brands is still at an early stage. Nestle has progressed more quickly than was anticipated at the time the recent management refresh. Both trade at a discount to their peers.

In contrast, the luxury goods sector we feel is priced far too highly. We sold out some years ago at prices that we thought excessive, particularly as many were acquiring competitors and complementary businesses at huge premiums, which has diluted their return metrics.

Australian Equities

Australian Equities Performance

Source: IRESS

In line with international indices, the Australian equity market produced another strong quarter, delivering 3.6% total return.

Notable during the quarter was a continuation of recent outperformance by value stocks as opposed to growth stocks. The strongest sector was the banks, very much a value sector, which started to outperform last quarter as it became clear that the economy was recovering strongly from the Covid-19 downturn. This was followed by telecom services as Telstra, recovering from a long period of underperformance, picked up steam.

Underperforming sectors included Infotech and Healthcare which are at extremely high valuation levels.

First half 2021 earnings results were announced by a large segment of the market.

The only major bank to report was CBA, which we regard as a good bellwether on the sector and the overall economy. Although the result remains covid-impacted, the picture is one of a strong recovery from the lows of 2020: cash earnings were up 32.2% from the previous half while loan impairment expenses more than halved.

The bank remains well provisioned against bad loans and we remain of the view that provisioning made during the early stages of the covid-induced downturn was done using very negative assumptions and which have not played out to date. At some point, we believe, CBA and the other banks will face the position of having to write these provisions back on to their accounts, providing a profit tailwind in the periods ahead.

An insight into the rapid nature of the recovery can be seen from the trajectory of active loan deferrals managed by CBA. As at June ’20 the total amounted to $51 billion, declining to a more modest $9 billion by January ’21, with the heavy lockdown state of Victoria comprising 47% of these. Our expectation is for further improvement in this number.

Telstra’s price performance has been disappointing for a while now, however we are starting to see the makings of better performance going forward. We have commented in previous notes around the attractive, concentrated industry structure as well as opportunities for product/service hikes as we transition from the old 4G technology to the new 5G.

During this quarter we note the significant announcement that Telstra will restructure its business under four operating entities: Infra Co Fixed & Infra Co Towers to house passive fixed and mobile telecom assets; Serve Co which will focus on products and services as well as the active parts of the network; and finally, Telstra International which will house the international businesses, including subsea cables.

We view this announcement as significant and paves the way for management to better realise the value of its asset base and provide monetisation opportunities. Perhaps more importantly, it signifies a level of seriousness in capitalising on the various value creating opportunities across the company as well as maintaining its 16-cent dividend per share.

Market valuation levels have moderated slightly but remain at extended levels. Outside financials and resources, large segments of the market are, in our view, overvalued and should be treated cautiously. Interest rates are a clear support for these valuations, but it should be noted that market-based interest rates have already started to move up from previously established record low levels.

ASX 200 – Latest 18.1x

Source: RIMES, IBES, MS Research

ASX 200 Industrials ex Financials– Latest 28.6x

Source: RIMES, IBES, MS Research

Interest Rates

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: IRESS

As Covid-19 vaccination programs begin to roll out global economic recovery is following, albeit at an uneven pace. The prospect of a third wave in Europe is causing some particular concerns for European recovery. Trade and commodity prices generally improved over the quarter but despite this inflation remains below central bank targets.

At its latest meeting, the Reserve Bank of Australia (RBA) maintained its target of 10 basis points for the cash rate. The initial $100 billion government bond purchase is about to be completed and the second $100 billion program will commence during April.

The RBA noted that the economic recovery is well underway in Australia but still expects wage and price pressures to remain subdued for some years. Accordingly, we expect Australian interest rates to stay at the current historically low levels for some years.

In the United States, the 10 year bond yield began to rise shortly after President Biden announced his stimulus package to help support the US economy recover post Covid-19, with the yield rising from under 1% at the end of December to a high of 1.7% in late-March. At its March meeting the Federal Open Market Committee (FOMC) stated that it would “keep interest rates near zero and maintain our sizable asset purchases. These measures along with our strong guidance on interest rates and on our balance sheet ensure that monetary policy will continue to deliver powerful support to the economy until the recovery is complete.”

Both the European Central Bank and the Bank of England have maintained their stimulatory monetary policies. Again, with inflation below target, interest rates will be held at close to zero for some time.

Property (REITS)

ASX Property Graph

Source: IRESS

The Australian property index was the underperformer in the March 21 quarter, down 0.56%, compared to the broader equity indices which posted strong quarterly gains.

As previously mentioned, the quarter has seen a market rotation towards more value-oriented stocks. The A-REIT index was no different. The rise of bond yields during the quarter is part of the explanation for this rotation.

The roll out of Covid-19 vaccine, coupled with the low case numbers has boosted the movement of people to a more normalized level. The previously gloomy outlook for the retail and office property sector is now seen as too pessimistic. This has seen the rebound of both sectors which has mostly traded at a huge discount to their Net Tangible Assets (NTA). Retail property names were mostly up – Scentre Group (1.4%), Vicinity Centres (3.1%), and Unibail-Rodamco-Westfield (4.9%). Dexus, one of the largest office property owners, was also up 3.7%.

On the other side of the spectrum, we have seen the reversal of property stocks that were exposed to growth and are trading at a big premium to book value. After a strong performance over the years, names like Goodman Group and Charter Hall Group were the unusual underperformers.

As things continue to normalize, we see the convergence in valuations set to continue. Markets will remain cautious on valuation, which should bode well for the value end of town.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Senior Client Relationship Manager with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright 2021 Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst