As at March 2022

Equity Market Returns

Source: IRESS

Investment markets declined sharply during the quarter, with the exception being the Australian market (up 1.6%). Global equities were down 8.2% (in Australian dollar terms) and Australian listed property was down 6.7%. Interest rates on cash were stable, however bond yield rose sharply with the Australian 10 year government bond yield rising to 2.8%. The US 10 year government bond yield rose to 2.5%, up from 1.5% at the beginning of the year.

Last quarter we commented on the changing inflation picture and that after a very long benign period there had been a sharp upturn, which central banks were being forced to acknowledge was no longer just supply chains re-starting after COVID-19. Subsequently, with the commencement of the Ukraine war, the outlook has worsened, particularly in the commodities directly affected: energy, fertilizers, grains and some industrial products.

A corollary to higher inflation is higher interest rates, which central banks have maintained at extremely low levels for the last 10-15 years. While this might be welcomed by savers who have been starved of low-risk income for over a decade, rates are still a long way below inflation, so in real terms the position is still not attractive.

Central banks have announced that they will increase short-term interest rates on multiple occasions during calendar 2022; the question is how many and how much. In Australia the RBA has announced it is also about to tighten.

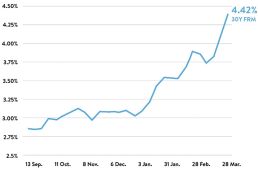

Below is a chart of US home loan rates since August, which shows that mortgage rates have risen sharply, from 2.8% eight months ago to 4.4% currently. In contrast, home loan rates in Australia have declined over the same period; a trend that we feel will must reverse. As we have discussed in earlier commentaries, rising interest rates will place pressure on valuations of assets that have been pushed up to levels that are high by historical standards. This effect will not be uniform and we feel there will be great benefit in holding assets that are not valued at extreme levels.

US 30 Year Fixed Rate Mortgage Rate

Source: Freddie Mac Primary Mortgage Market Survey

On the positive side, of great benefit to Australia has been the sharp rise in commodity prices, particularly iron ore, coal and agricultural commodities. As an indication of how beneficial this has been, the balance of payments has risen to an excess of $125 billion in the last year, reversing over 30 years of negative figures. One result of these rises has been the enormous increase in profitability of resource companies, which has been accompanied by extremely large franked dividends from the December profit announcements. The dividend yields of these stocks is in excess of 10% (annualised) for the majors, BHP and RIO, to above 20% for some other producers. We think these dividends will be repeated for the June profit announcements (please see comments below in the Australian Equities section).

Additionally, in the finance sector, rising rates are starting to improve the margins of both banks and insurance companies. In moderation, increasing rates widen the gap between what banks pay for deposits and what they earn on loans. This is reversing a long period when the margins have been under pressure.

International Equities

International Equities Performance

Source: MSCI

Global markets declined sharply during the quarter, the MSCI, a global index of stocks declined 8.2% in Australian dollar terms as a number of factors took hold. However, many of the stocks held widely in the portfolios were either up or steady. This was particularly the case in the following sectors: financial, healthcare (pharmaceuticals and hospitals), manufacturing, waste management and Alphabet.

The rise in global bond yields, which tend to adversely affect valuations, weighed heavily on highly priced growth sectors, principally the tech sector, where declines were very significant. Additionally, disruptions to supply chains, which developed during COVID-19, were exacerbated by the Russian invasion of Ukraine. This was particularly pronounced in industries producing consumer durables such as autos, where the supply chains are extremely complex and susceptible to the weakest link effect.

This has limited production for companies such as Volkswagen and Lear Corporation (two widely held stocks). It is not expected that the shortages will be alleviated quickly, and production will be at lower levels for some time. Demand however remains high, and we think that sales are deferred rather than lost. However, the valuations of these companies are very modest and do not reflect high expectations; as a result, we are comfortable holding them and are looking for opportunities to buy other undervalued stocks.

The healthcare sector, which we have long felt is undervalued (in contrast to the Australian equivalent), has proven resilient. In the pharmaceuticals industry the major investment is in Merck (Sharp & Dohme); earnings have grown strongly over the last five years (average 27% p.a.) and are expected to continue to grow from the success of their oncology portfolio. We find the company’s long history of research success and their acquisition strategy attractive.

Merck tends to acquire biotech companies with specific drug candidates rather than do mega mergers. We feel prices paid in big mergers are, more often than not, too high and invariably presents numerous and complex integration problems.

The other major holding in the sector is Universal Health Services, a hospital operator, which is very attractively priced. We are also building a position in Quest Diagnostics, which is one of the two dominant pathology services firms in the US. While revenue has been inflated since COVID-19, the share price we feel has now discounted this unusual situation and reflects good long-term value. Both these investments we think of as having utility characteristics, which will not be greatly affected by negative periods in the economic cycles. Most importantly are attractively priced, with an underlying return we estimate of in excess of 12%. This appears to us to be a very good return for the risk being taken.

As mentioned in the overview, we find the financial sector attractive as prices of the major banks and insurance companies are extremely low particularly in relation to the level of earnings on their capital. These earnings are tending to improve as interest rates rise. For banks, the margins tend to increase as cost of deposits lag the yield on mortgages and other loans (please see the graph in the overview). Similarly for insurance companies the earnings on their investment books also improve, and at this time, premiums are also rising. The investments in Wells Fargo, Lloyds, Allianz and Travelers (both insurance companies), appear very attractive.

We retain an intense focus on valuations in the global portfolio as rising interest rates are placing question marks against some of the excessive valuations that have arisen during the last five to six years because of loose monetary policy. There are, we believe, numerous areas where the valuations are attractive and will be less adversely affected by interest rate rises.

Australian Equities

Australian Equities Performance

Source: IRESS

The Australian equity market has proved to be more resilient than most over the quarter with the broad-based All Ordinaries index returning 1.62% over the quarter.

The resource sector performed strongly as commodity prices continued to be well supported by global demand. Further, the war in Ukraine and resulting boycott of Russia by western countries has produced an unexpected price spike across a range of commodities including minerals and metals as well as energy.

BHP and Rio each produced another exceptional set of results. BHP reported record first half earnings of USD 9.7 billion, up 57% from a year ago. This result was led by iron ore where strong Chinese demand and tightness in supply continue to support prices of over USD 100 per tonne. Price strength has been a factor across a broad range of commodities, with the copper and metallurgical coal divisions providing a meaningful contribution. Dividend distribution was a highlight with the company announcing a 49% hike in dividend to 150 US cents per share.

Rio’s results were similarly impressive with underlying earnings up 72% and dividend up 88%. The double-digit dividend yields produced by both companies have proved extremely attractive in the low-rate environment, and even more so with the benefit of franking credits.

Remaining in the commodity space, our newly acquired coal stocks produced a superb set of results. New Hope and Whitehaven are thermal coal producers and are benefitting from record high prices. We have been of the view that demand for thermal coal remains healthy in key export markets in Asia. At the same time supply side constraints provide a medium-term opportunity for these producers to generate highly attractive returns. Both companies have very strong balance sheets with either no debt (NHC) or fast reducing debt (WHC), allowing for strong returns to shareholders from dividends and special dividends – a common theme currently in the resource space. The full year results show promise for further attractive returns to shareholders on the back of disruption to global energy markets from the war in Ukraine.

Discretionary retailers Harvey Norman and JB HiFi announced strong half year results during the quarter. Both companies are benefitting from strong discretionary retail spending over the COVID-19 period. Consumers have been buoyed by a strong economy and jobs market and have been further supported by generous government support measures. At the same time, some alternative avenues for retail spending have been cut, such as overseas travel. The rebuilding required after the floods in NSW and SE Qld adds to an already healthy demand outlook.

Portfolio bank holdings did not produce earnings results during the quarter (CBA was the only major to report), however we refer to comments made last quarter regarding a more favourable environment for bank net interest margins as market interest rates move higher. Over the quarter we saw 3-year rates spike 1.45% to 2.33% whilst 10-year rates rose 1.14% to 2.83% This provided a positive queue to bank stock prices with ANZ, NAB and WBC each bouncing sharply off their quarterly lows.

Life insurer Noble Oak continued its strong run post IPO with underlying profit up 47% versus same period a year ago. Management point to in-force premium growth – their preferred measure for value generation – growing at 59% over the year to $226.5 million, ahead of prospectus forecasts.

At this point, the conclusion is that the Australian economy has weathered the COVID-19 shock better than most. Although it is early days, it appears likely the same applies to the follow-on shock of a new war in Europe. Government forecasts Australian mineral and energy exports to top $425 billion for this fiscal year – a record.

Interest Rates

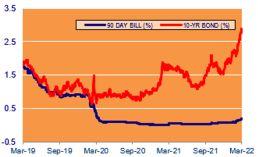

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: IRESS

The Reserve Bank of Australia (RBA) maintained the cash rate at 10 basis points at its April meeting but in its commentary dropped the word ‘patient’ so that we now expect a minimum 15bp rate increase by the June meeting. Significant further rate rises are expected over FY23 as inflation takes hold in Australia. Over the quarter, market rates moved higher with 90 day bank bills moving from 0.07% to 0.23%, 3 year Government Bonds 0.88% to 2.33% and 10 year Government Bonds 1.61% to 2.83%. These rates are also expected to rise over the next financial year.

At its March meeting the US Federal Reserve, (the Fed), raised the Fed Funds Rate 25bps and market expectations are that the rate will be 2% by the end of 2022. Given the tight labour market, supply chain issues and sanctions on Russia pushing up commodity prices the prospects for higher inflation have increased markedly since this meeting and hence the prospect for higher interest rates. As a consequence, the quantitative easing cycle is over and will be replaced by quantitative tightening as the Fed reduces its balance sheet.

The Bank of England again raised the Bank Rate during the quarter, and it is now 0.75%. With inflation currently at 6.2% in the UK the Monetary Policy Committee (MPC) noted that ‘modest tightening in monetary policy may be appropriate in the coming months.’

The European Central Bank (ECB) has held rates at 0.0% but with inflation rising rapidly, especially in Germany, we expect rates to rise over the remainder of 2022.

Property (REITS)

ASX Property Graph

Source: IRESS

After a strong run from the COVID-19 lows in March 2020, the A-REITs index have given up ground, posting a negative 6.7% return for the quarter.

As mentioned earlier in the commentary, bond yields rose sharply during the quarter. The interest rate backdrop is creating headwinds for real estate in terms of valuation, as the sector has always been viewed as defensive and used as a bond proxy. Historically, A-REITs underperform in periods of bond yield escalation, with valuation de-rating for the sector typically occurring concurrently when bond yields go up. During the quarter, the Price Earnings (PE) multiple of the A-REIT index has compressed to ~17x, down from 19x last year.

However, despite the recent increase in bond yields impacting valuations, the secular tailwind for industrial real estate remains, and the returning to work, from COVID-19 lockdowns, has also provided something to cheer for in the office market, whilst the appetite and abundance of dry powder identified for real estate investment also provides a solid backdrop for property fund managers.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright 2021 Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst