As at September 2021

Equity Market Returns

Source: IRESS

A broad range of asset prices rose strongly during the year. As can be seen from the table above, globally, equities prices were up nearly 28% in $US terms and in Australia over 30%. Residential property prices were also up extremely strongly, as has been widely reported, and has started to cause concerns in many markets, with efforts being made to limit rises.

This has not, to date, involved raising interest rates on cash which remains at historically low levels in developed economies. Bond yields have, however, risen by approximately 1.2% from the lows of 2020, but they too remain at extremely low levels and well below current inflation levels. Economic growth in most economies is high (6.0% in the US, 5.3% in China, 4.8% in Europe and 3.8% in Australia) and unemployment levels low (excluding Europe). Governments are running high or very high budget deficits with little sign of this fiscal stimulation being moderated (in the US it is increasing). Also, there are only muted indications that central banks will moderate the very loose monetary policies they have been running.

As a result of all this stimulus, concerns are rising that the central banks’ assertions that the inflationary spike is not as temporary as they thought and that the punchbowl has been spiked rather than been taken away as it should have been.

(Ancient quip: central bankers always take away the punch bowl just as the party is getting going).

Supply chains may be only now spluttering back into action, but there are a number of other worrying signs: rising wages and labour shortages, increases in commodity prices both agricultural and industrial, which are feeding through to consumer staples, and importantly energy prices. This perhaps is important as it tends to have a powerful effect on inflationary expectations. Energy prices have increased as a result of gas shortages and low oil production levels as well as the transition of electricity grids from traditional generation to intermittent sources. This is proving more problematic than consumers have been led to believe and is starting to have widespread effects on industrial production (particularly in China). The issues may become more pronounced during the northern winter.

Interest rates are now well below inflation rates and the question might be asked how long will investors be willing to accept negative real returns, particularly for very long-dated securities? The 30-year US government bond has a yield of 1.8%!

We retain the view that the assets most at risk are those where the pricing is the most elevated. Consequently, the core stocks in the portfolios are in sectors where pricing is modest. Indeed, the finance sector (both banks and insurance) may benefit from modestly higher rates as their margins have for some time been compressed by extremely low interest rates (and a flat yield curve).

International Equities

International Equities Performance

Source: MSCI

International equities markets were unchanged in $US for the quarter (although up 3.9% in A$) and up 27.8% for the year as measured by the MSCI (an index of global markets), expressed in Australian dollars.

Equities markets rose strongly during the last twelve months, although the last three months saw the rate level off as fresh concerns arose over the spread of the Covid Delta strain. Additionally, there was pronounced weakness in China stocks over concerns of increasingly overt political involvement in capital markets. The long running sore of the financial troubled property developer Evergrande also came to a head, focussing attention on excesses in property and on banking troubles, periodic themes in China.

We would like to re-emphasise that the focus of our strategy remains to limit portfolios’ exposure to stocks where valuations are stretched. For some time we have been reducing the holdings in companies such as Microsoft, Alphabet (aka Google) and more recently Eli Lilly. Each are attractive companies, but we feel we have already earned most of the return that will be available for many years to come. Re-investment has been directed to sectors and stocks where we think valuations as well as the company itself are attractive. As has been mentioned previously the differential between the valuation of in favour and out of favour stocks and sectors is unusually large. This has thrown up a number of attractive opportunities.

One area we think is looking attractive is the telecommunications sector. After a period of heavy investment to roll out 5G networks and acquire spectrum there appears to be improving revenue growth and returns for the better placed operators. Returns are improving, mainly as a result of increases in prices to consumers; we feel that this has some way to go as there seems to be more rationality in competition between the players (they do comment that competition is intense, but nevertheless, prices are being raised). There is also the prospect of expanded markets in communication between devices (IoT), although we are treating this as an additional benefit rather than the base case. We think that this could develop in a similar way to the last technological change over approximately ten years ago. Stock prices are very attractive.

Portfolios have long held the major pharma company Merck Sharp and Dohme, best known for their dominant oncology drug Keytruda. Topically, the company also has a large vaccine business, one of the major successes in this area has been Gardasil, which was co-created by Australian Ian Frazer, and has dramatically reduced the incidence of cervical cancer. While it was disappointing that their Covid vaccine trials failed they have recently announced success with an antiviral drug which was found to reduce hospitalisation and mortalities by half in vulnerable populations – a significant development in reducing the pressure on hospital systems of future outbreaks.

Even after the strong recovery in share prices in the banking and insurance sectors, we think that the prices are still attractive. The recent results (in mid-October) from Wells Fargo show improved underlying returns and improvements in efficiency. Additionally, there were more writebacks of the provisions made early in the crisis. It is now apparent that much of the provisioning was not required as the lending books were in good shape. The share price of neither Wells Fargo nor Lloyds, another core holding, have yet to reach pre-Covid levels. In our view the share prices of these banks have yet to fully adjust. The core portfolio holdings in insurance stocks, Travelers Cos. and Allianz are also very modestly priced.

While at the current price we are no longer adding to positions in Nestle we are encouraged by the strong operating performance, after the company had repositioned its portfolio under Mark Schneider. Organic sales growth (that is growth excluding acquisitions/disposals of brands) for the first 9 months of 2021 was up 7.6% with margins maintained at 17.5% was an excellent result. Of particular note was the performance of petfood and coffee.

VW, which vies with Toyota as the largest vehicle manufacturer, and produces a range of cars from the utilitarian Golf to the extrovert Porsche and Lamborghini is the most advanced of the large vehicle manufacturers in the development of electric vehicles. This is vital as the electric vehicles are moving to dominate vehicle manufacture. Despite the problems of chip shortages that have had a significant adverse effect on the industry and on VW we think the outlook is promising and the valuation of the company is extremely attractive.

Australian Equities

Australian Equities Performance

Source: IRESS

The fallout from the Covid-19 pandemic and resulting lockdowns continue to have a major impact on the Australian economy and equity markets. At an aggregate level, the domestic economy has performed better than expected with GDP recovering to pre-pandemic levels and employment reaching record levels. Much of this strength of course, can be attributed to accommodative fiscal and monetary policy: public sector consumption to as much as 22% of GDP versus a pre-pandemic level of around 18%. At the same time official interest rates have been pushed to an all-time low of 0.1%. With lockdowns reinstated in NSW and Victoria (but now lifted) we can expect further disruption ahead, but the experience so far suggests the fallout is being well managed.

One thing is clear, 18 months into the pandemic there have been significant winners and losers in the process. The suppression of interest rates coupled with the homebuilder support program has led to record approvals for housing construction, as well as alterations. Building products company CSR has been a direct beneficiary of this with its pipeline being extended across CY21-22.

Newly added stocks Harvey Norman and JB HiFi have also benefitted through their household appliance and furnishings exposure. JBH’s The Good Guys, for example, saw double digit growth of 13.7% in sales for FY21 with strong growth in key categories of refrigeration, floor care and appliances. Harvey Norman has seen similarly strong results, reporting record earnings for FY21, partly off the back of double-digit sales growth from its domestic franchise network: sales outside of the lockdown affected fourth quarter, more than offset the negative effect from the restrictions.

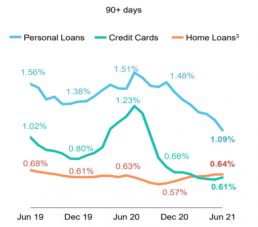

CBA’s result also provides valuable insight into the performance of the domestic economy and on most measures the readings are encouraging. Importantly, the bank’s loan book credit metrics have fast recovered and in some cases are now better than pre-pandemic levels – see personal loans arrears and credit card arrears in the below chart from its recent annual result.

CBA Lending Arrears

Source: CBA

The bank is seeing the impact of the housing boom with a surge in lending for new and existing dwellings; home lending for FY21 was up a hefty 33% to $141 bil. We have seen similarly strong results from the other 3 major banks reporting their quarterly market updates.

Against this backdrop the ASX surged to a peak just shy of 7,900 points before surrendering most of the gains to finish at 7,630 for the quarter. At this point we believe PPM’s focused approach to valuation is especially important. Clearly, a direct effect of the extraordinary support measures provided by the government and RBA has been an inflation of asset prices across the board, including property and equities. Although we wouldn’t argue that there is a general bubble in the equity market there are clearly pockets of great overvaluation – particularly in technology. But, as is evidenced by recent portfolio purchases – HVN, JBH, WOW, CWY, ELD – reasonable value in good quality businesses remains available.

The commodity space continues to be interesting from a price point of view. A number of key commodities continue to perform strongly and, in some cases, have moved to record price levels – coal for example. On the other hand, iron ore prices have pulled back sharply after reaching record prices of over USD200 per ton. We have maintained our exposure to diversified miners BHP and Rio given that our assessment of value was made off long term normalised iron ore prices in the $70-80 per ton range. Both companies have extremely strong balance sheets with the outlook for distribution to shareholders remaining attractive. BHP, for example, has distributed over $4 to shareholders of the past year, a yield of 8.3% from its June 30 share price.

PPM’s rural commodity exposure is also benefitting from another buoyant season. Good rainfall across many of the key producing regions in Australia means the volume outlook for crop and livestock production is very encouraging which, combined with attractive soft commodity prices, bodes well for stocks such as Elders.

Interest Rates

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: IRESS

As the world emerges from the impact of Covid-19 governments are tentatively beginning to talk about reducing fiscal stimulus policies and Central Banks are hinting that inflation is beginning to increase, although most are suggesting it will be transitory, a view we do not completely share.

Over the quarter, interest rates remained at historically low levels, however the narrative from central banks has begun to change. At its most recent meeting the US Federal Reserve (the Fed) left the federal fund rate (FFR) unchanged but noted that it could need to lift rates as early as 2022 and implied that the FFR could be 1.8% in 2024. On tapering asset purchases, the Fed noted that “a moderation of asset purchases may soon be warranted.” Chairman Powell was quoted as saying the tapering process could start as soon as the next meeting and conclude in 2022.

The Bank of England Monetary Policy Committee (MPC) has maintained the Bank Rate at 0.1% and confirmed its bond purchasing. The MPC expects inflation to exceed 4% in the current quarter and consequently a lift in the Bank Rate in 2022 appears likely.

The Reserve Bank of Australia (RBA), at its latest meeting maintained the cash rate of 0.1% and the bond yield at 0.1% for April 2024 Australian Government Bonds and will continue to purchase government securities at the rate of $4 billion per week until at least mid-February 2022. “It will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range …which will not be met before 2024.”

Ten-year Government bonds are currently trading at 1.52% in Australia and 1.53% in the United States.

Property (REITS)

ASX Property Graph

Source: IRESS

The A-REIT index was up 4.8% in the quarter to September. This has added to a very strong run since the COVID-19 impacted market correction in 2020, with a one-year total return of 30.7%.

The recovery, however, has been uneven, with property fund managers and industrial companies leading the charge, whilst the least favourable sectors like office and major retail shopping centres continuing to be laggards. Nevertheless, the whole sector has rebounded from its lows. Owners of niche or alternative assets including pubs, petrol stations, convenience stores, farms, childcare centres, holiday parks, build-to-rent homes, self-storage, data centres and cold-storage facilities, are also trading at a very high level, with a lot of them now trading at or above their net tangible asset backing (NTA).

Appetite for the sector has been very strong, both in the listed space and private markets, as the chase for yield in this low interest rate environment continues. During the quarter, there were a number of capital raisings to fund major acquisitions including: Centuria Industrial REIT ($300m), Dexus Industrial REIT ($350m), and HomeCo Daily Needs REIT ($88m). While Home Consortium (HMC) IPO-ed its healthcare related properties into the HealthCo Healthcare and Wellness REIT (HCW), which attracted a lot of support from the market.

Whilst the recovery and appetite for the sector has been strong, uncertainties remain, mostly with the lockdowns in major states during the quarter. The recent results show the reluctance of many listed players to provide earnings guidance. The increase in bond yields towards the end of the quarter has also shaken the market, including A-REITs. This serves as a good reminder to stay focused on valuation and be a bit more selective with future opportunities.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Ian Hardy

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager

Max Herron-Vellacott

Analyst

Neil Sahai

Dealer / Analyst