Retail – Double digit Growth!

A discussion by Hugh MacNally, Chairman and Founder of Private Portfolio Managers

An aspect of PPM’s investment philosophy is a belief that even in difficult industries great companies continue to succeed and there is a good chance that they will be attractively priced.

With all the concern about the retail sector (Amazon, high household debt and low wage growth, low growth in turnover and excess floor space) it seems a pretty unlikely place to find a company that is doing well and thus in a perverse way a good place to look (Templeton would approve1).

In luxury goods the story over the last eighteen months has been one of growth in defiance of the wider trend.

LVMH (Louis Vuitton Moet Hennessey) is the owner of a large number of high end luxury goods brands from wine, couture and accessories to luggage. In a number of product lines the company is vertically integrated from raw material source to retail shop and retains a tight control over all aspects of the value chain. It grows grapes in super premium areas, makes wines and then markets them. Loro Piana, the maker of beautiful knitted garments, grows their own cashmere and vicuna to ensure supply and quality of fibre. The leather goods, fashion and accessories that it manufactures it sells through its own stores which number nearly 4,000 from Paris to Phnom Penh.

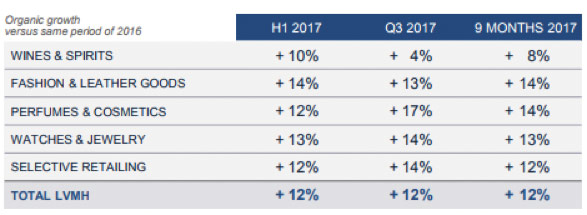

In this difficult market, LVMH sales for the year to date were up 12% as indicated in the table below, with all the five business groups all recording growth above 10%, except wine and spirits (which was constrained by volume!) Watches which had suffered from reduced Chinese demand for a number of years recovered strongly.

LVMH Sales by Product Group

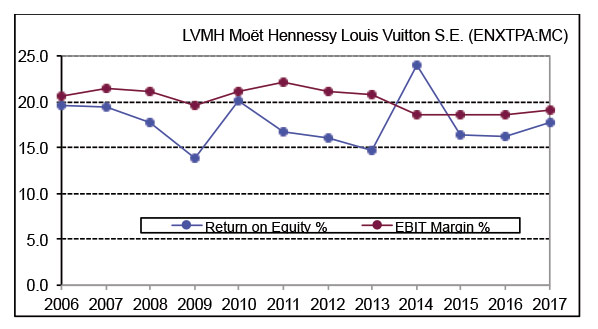

What is interesting about the company is the stability of the margins they have earned. As can be seen, in the following chart the EBIT margin (an important measure of profitability shown in red) has remained relatively constant at around 20% over the last 10 years. What is also interesting is the return on equity (In blue – an important measure of the long term return shareholders will receive) has also been between 15% and 20% despite all the acquisitions. It might be noted that overpriced acquisitions have been the most consistent destroyer of corporate equity returns since ‘Adam was a boy’. Indeed in the early days LVMH made an array of acquisitions that looked pretty shaky (There was even a Harvard Case study putting Bernard Arnault, the CEO, on the protagonists spot over this issue).

LVMH continues to be acquisitive, buying and selling over 30 assets over the last 10 years. Most of the acquisitions have been quite small but some of the larger acquisitions have been: an ultimately unsuccessful raid on Hermes in 2010 (17% holding subsequently disposed of), Bulgari in 2011, Loro Piana in 2013 and this year Christian Dior.

LVMH Return on Equity and EBIT Margin %

Why has LVMH been so successful in such a bad retail environment? A few suggestions for a bigger case study: disciplined approach, having an obsession with quality and the meaning of the brand, not oversupplying the market, not devaluing the brand for the sake of short-term profit, an effective management style, decentralised not inhibiting the artistic freedom of brands but giving them capital and support. The company also seems to have learned from its mistakes, firstly, from the early acquisition strategy and more recently from a too aggressive retail store expansion in China.

1 John Templeton was one of the most successful portfolio managers of the C20 and had a strategy he called “maximum pessimism” or buying when there were only negative views.

Print this Article