As at June 2023

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

During the last year we have seen sharply rising interest rates, high inflation, slowing economic growth and political tension. And very high returns in equities markets as can be seen in the table on the preceding page: the MSCI, a global index of stocks, was up 16.5%, the Australian market was up 14.8% and other markets, except for China and the UK were also up strongly. So much for the value of macro-economic analysis in picking stocks!

It is counter intuitive, but the average return in equities markets from period immediately prior to the appearance of Covid, to date has been close to the long-term average, despite the wild swings during the period. Averages are however often misleading and over this period we have seen a variation between industries. The volatility in popular sectors has been particularly high; in the tech sector we have seen valuations go to extremes not seen since the tech bubble of 2000 and then fall 60-90%, only to rise very strongly in the last year. The businesses of many of these companies were very attractive (high returns on capital and strongly growing revenues) but the valuations were excessive – however, there was a brief period in late 2022 when both business and valuation were attractive.

Conversely, the valuations in sectors such as healthcare were very modest by historical standards for a long time and have only recently recovered in the market’s esteem. In the table above the returns from the healthcare stocks have mostly been very high. The portfolios have generally focussed on US healthcare stocks as the domestic companies have been, in our view, too expensive to buy for many years. Great companies like Cochlear and CSL are examples.

Perhaps the odd sector out has been the finance sector, which we have regarded as inexpensive, but it has remained so for a long time. Again, looking at the table of prices there is a wide range of returns for both domestic and global stocks, but on average the returns have not been high and certainly not what we had hoped for. In an unfortunate earlier observation, we pointed to the conservative lending practices of banks over the last 7-8 years as a strength, only to be ambushed in March by an unusual banking crisis; one not caused by bad debts, but rather by liquidity issues. While this has not affected the major commercial banks it does, in our view, change the economics and we have adjusted our valuation range downwards. The banks we hold are at low valuations currently, but our expectations of returns are now somewhat diminished.

In the nature of counter intuitive investments, portfolios are holding positions in consumer discretionary stocks such as Harvey Norman and JB HiFi domestically (we are looking at situations that might be attractive for global exposures). Our view is that the prices of these stocks have fallen so far that they have discounted a very major downturn. We think that we have acquired them at returns on equity that are extremely attractive (average returns, not those boosted by Covid buying). JB HiFi’s share price has done the better of the two, but we think that Harvey Norman, which is valued at little more than its property value, is very undervalued.

While these two stocks share prices have had a difficult time recently, we would contrast this with the performance of another sector which might equally have been viewed negatively. Building materials and home building stocks, James Hardie, CSR and DR Horton have all done very well this year being up 24%, 28% and 84% respectively. The contrast with JB Hifi etc seems illogical and in the end, we think all these companies will do well. The depressed value of the consumer stocks has presented an opportunity.

In a similar vein the holding in Elders, which Peter discusses below, is extremely attractively priced. As can be seen from the price sheet above, the share price has fallen almost 50% for the year, partly influenced by the fall in agricultural prices we think or perhaps views that another drought is about to start. This undervalues an extremely well-run company by a substantial amount in our view.

A number of sectors of the market have become expensive or extremely expensive. Anything associated with AI is an example; this includes such stocks as Nvidia, which we like, but not at these prices. However, there are some attractive areas in semi-conductors where the emergence of oversupply has created opportunities.

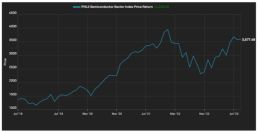

Short term interest rates increased during the quarter, after the banking issues of March, and central banks have indicated that the “pause” is likely to be temporary. Longer term bond yields however are at the same level they were a year ago and have been in within a band of about half a percent for over a year.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global equities markets rose strongly with the MSCI, an index of global stocks, rising 16.5% for the year and 6.3% for the last quarter. As can be seen from the chart above, which covers three years, markets are well above the lows reached at the start of Covid, but still below the highs of late 2021.

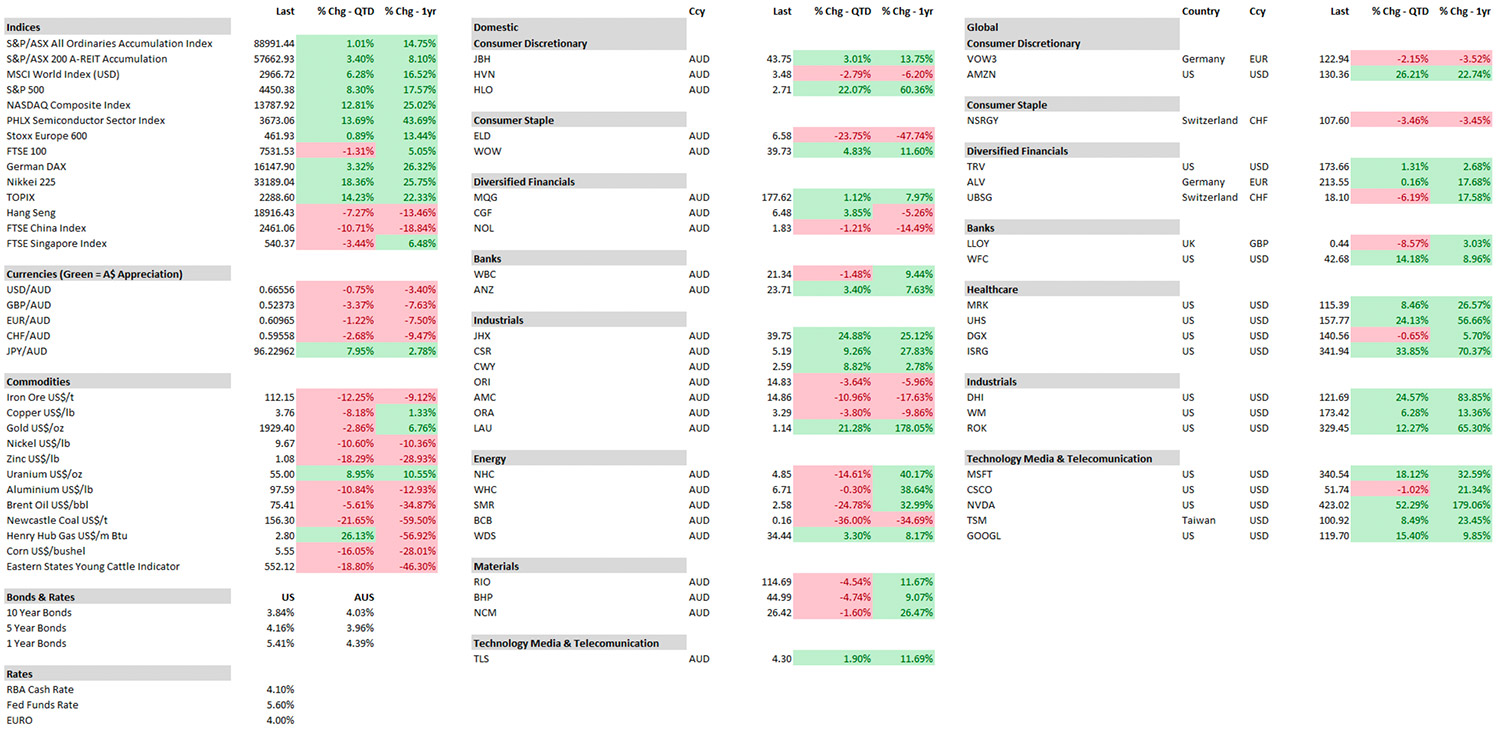

Technology Stocks continued to rise during the quarter; those involved in AI were major beneficiaries. The increases were most pronounced in software producers, high end chip manufacturers and internet infrastructure (such as data centre operators). While there have been falls in price of general-purpose chips as supply again exceeded demand, the manufacture of high-end chips has been robust. The main exposure is Taiwan Semiconductor Manufacturing Company, which is the dominant producer of high-end chips. While the finished product comes from Taiwan it results from an immensely complex web of specialist suppliers from all over the globe. The level of specialisation is so pervasive that chip manufacture is difficult to re-locate and offers some protection to the established manufacturers.

Despite the oversupply and falling prices in chips, the closely watched index of semiconductor suppliers, the Philadelphia Semiconductor Index rose nearly 40% over the year (see the table on the previous page).

The industry has some of the characteristics of commodity markets, huge amounts of capital invested and a supply/demand balance that swings from surplus to deficit regularly. Nevertheless, the returns have been very high for investors for over 20 years. The areas in which we are interested are the high-end chips. As has been the case in many industries the top end is where all the margin is and TSMC is the Hermes of chips.

Philadelphia Semiconductor Index – 5 year

Source: S&P Capital IQ

In another part of the industry, chip and software design, Nvidia has a dominant position in the supply of chips required for AI and machine learning. While we like the company, the rise in the share price over the last year makes it no longer attractive from a valuation perspective. While this company has ceased to be on the investment horizon, we think there are other opportunities that will emerge, as this is a very dynamic industry.

Turning to healthcare, Merck (MRK) continues to perform well with growing sales in Keytruda, their key oncology drug. A major focus is to increase the range of patients for which the drug has efficacy (currently only 25-30% of patients) by finding combinations of drugs that work. One promising combination is produced by Moderna (MRNA, best known for its Covid vaccine). The technology that resulted in the Covid vaccine was originally intended for other purposes, one of which was oncology. Recently, MRNA published impressive results from a clinical trial with Merck. As a result of their success during Covid MRNA now has cash holdings of US$16 Billion, which is funding a wide range of programs and which we feel makes the company attractive.

The operational performance of Universal Health Services (UHS) has been improving slowly over the last year. The problems of shortages of labour and distortion to the established patterns of demand were common to many service industries, which are now moving closer to the norm. Prior to Covid UHS had a long history of utility like returns, something that we feel is now re-asserting itself.

The difficulties of the finance sector have remained. After a brief period of recovery, the banks had another difficult period. The quarter introduced an unforeseen issue of liquidity. This brought down one bank with an impeccable lending record and forced the sale of Credit Suisse to UBS. The lesson we take away from this is that the pricing of financial stocks must be lower than we have hitherto required, as the inherent risks are now higher. The risk that social media driven on-line withdrawals was demonstrated in March where the speed of withdrawals can now be an order of magnitude (or two) higher than was the case when a physical appearance was required for withdrawals.

Insurance has done better, but the results have not been brilliant.

It is interesting that housing, one of the industries most affected by rising interest rates, had a spectacular return over the last 12 months. DR Horton (DHI), a company that portfolios hold, continues to perform well. Although returns on capital are below the extremely high levels of the recent past, they are still very attractive. As we have commented before, the demand for housing in the US, UK and Australia is very high and this would seem to bode well for well-run companies like DHI.

Through no particular design, the portfolio’s global exposure is dominated by the holdings in US companies. We have not expressly looked for US companies it is rather that the investment selection process throws up US companies the most. Despite the political chaos of the recent past, the business of America still seems to be business.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Capital IQ

The Australian equity market rose 14.8% for the year ended 30 June with 1% coming in the final quarter.

At this point in the year, it is worthwhile reviewing sector performance over the fiscal year ended June 30. Sectors showing strongest performance included information technology; materials; utilities; communications; and energy. Underperformers included healthcare; real estate; and consumer staples. It is interesting that despite a weaker outlook for global growth, resource-related stocks continued to perform, whilst typically defensive sectors such as healthcare and staples underperformed the market. Financials were in line; consumer discretionary slightly under market.

Three of the four major banks (ANZ, NAB, WBC) reported first half results during the quarter. The three majors each continued steady performance with a normalisation of results versus three years ago. Loan growth remains moderate, around 4% for home lending; business loan growth a little higher. Whilst lending margins have lifted, they are showing signs of tapering, led by NAB on the back of strong deposit competition. ANZ and Westpac are yet to show a decline, but management are indicating a peak in margins has been reached.

We observe that competition in the sector remains strong and that with a slowing economy loan demand will be pressured along with an increased risk of higher bad debts. We will maintain our underweight position in the sector, with a focus on the cheaper end – ANZ and Westpac. We have reduced our position in Macquarie Bank on valuation grounds but will, for the time being, maintain some exposure due to the bank’s growth opportunities. NAB and CBA, we consider, too expensive to hold unless there is a large unrealised capital gain attached to the position.

Despite the rising interest rate environment, our housing related exposure produced strong returns over the quarter and fiscal year. CSR, our domestically focused building materials company, delivered strong full year earnings results. Building products revenue growth of 14% flowed through to 20% EBIT growth (earnings before interest and tax), a solid performance. The company is experiencing strong demand for key products such as Hebel panels and blocks and gyprock plaster board, while pointing to a strong order pipeline as commencements exceed completions. The company’s landbank provides additional investment appeal.

Elders has been a long-held position in our portfolios providing high quality exposure to the Australian agricultural sector. The company, over many years, has built a well-diversified business in terms of geographic spread as well as commodity exposure. This is important in helping the company manage inherent volatility in the industry.

Management has the right focus in terms of return on invested capital and looks to deliver compelling returns through the cycle: satisfactory in lean years, highly attractive in good years.

First half results showed the company cycling one of its intermittent weak periods as several key commodity prices retreated from historic highs the previous year. This position was exacerbated by flood events on Australia’s east coast and northwest regions. Thus, although sales rose 9% in the half year, margins declined across most business lines on cost pressures and the lower commodity prices.

Despite this, the company produced a return on capital of 16.9%, above its hurdle of 15%. Positively, the management guided to full year EBIT (earnings before interest and tax) of between $180mil – $200mil. If achieved at the top end, this will represent only a modest decline from the previous year’s record.

With Elders now trading on a single-digit price earnings multiple (8.7X for FY23), we believe the company represents attractive value at current prices.

Switching now to broad market valuations, given we are sitting at the start of the new fiscal year, we observe the price earnings multiple for the ASX200 as a whole is approximately in line with long term average levels – 14.5x prospective (FY24) earnings.

ASX 200 12mf Price-to-Earnings (Latest = 14.5x)

Source: RIMES, IBES, Morgan Stanley Research

Against this, we can confirm that we are still able to identify investment candidates able to deliver a return in excess of our 10% hurdle rate. Thus, although we have headwinds including rising interest rates, high inflation and slowing economic growth, the prospects for equities remain attractive, in our view.

Interest Rates

Ian Hardy

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

After 500 bps of rate hikes the US Federal Open Market Committee (FOMC) paused interest rates at its June meeting and has maintained the Federal Funds rate in a range of 5 to 51/4 percent and continues to reduce its securities holdings. In essence the FOMC wants to see the full effects of its tightening to date given “the uncertain lags with which monetary policy affects the economy”.

Looking ahead, the Committee’s view is that further rate increases will be appropriate this year to bring inflation down to within the target range over time. Later in the press conference after the FOMC meeting it was disclosed that participants in the FOMC project a Federal Funds rate of 5.6 percent by the end of this year.

At its last meeting in June the Bank of England (BoE) lifted the cash rate by 50 bps to 5 percent. This was twice the quarter point rise the market was anticipating and there are indications that a rate above 6 percent will occur early next year as inflation remains stubbornly above 8 percent, way above the BoE 2 percent target!

The Reserve Bank of Australia (RBA) did not follow the BoE and has left the Cash Rate unchanged at 4.10 percent, as it awaits economic indicators as to the effect of rate rises to-date. It did however conclude its statement by saying “some further tightening of monetary policy may be required.”

It is worth noting all three Central Banks used words such as “do what is necessary”, or “whatever it takes” to bring inflation under control, suggesting further rate rises may occur.

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Capital IQ

The Australian A-REIT index bounced back 3.4% during the quarter, outperforming the broader All Ordinaries Accumulation Index. However, for the full financial year ending 2023 (FY23), the A-REIT index is still lagging behind, posting an 8.1% return for the financial year.

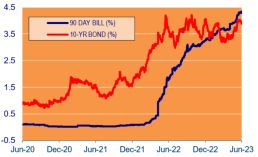

Mirvac Group (MGR) and Stockland (SGP) were the two best performing stocks from the sector during FY23, driven largely by a very strong residential property market. However, multiple succession of interest rate rises may have an impact on demand going forward, mostly as mortgage repayments now make up on average close to 40% of income.

Mortgage share of income shows affordability at record low levels

Source: ABS, Macrobond, CoreLogic, UBSe

On the flipside, both Mirvac and Stockland are venturing into the Build-to-Rent market. While the Build-to-Rent strategy could be a good one, as more people are priced out by high property prices, the return on capital potential and scalability of the Build-to-Rent remains to be seen.

Several listed players have given their updated property valuations and capitalisation rates for their properties during the quarter. Expansion of capitalisation rates and decreases in asset values have been the common theme. Dexus (DXS) recently announced that an independent valuation conducted has resulted in a decrease of $1billion (6%) compared to the December 2023 book value of their assets. The weighted average capitalisation rate across Dexus’ portfolio expanded by 32 basis points over the past six months, from 4.80% at the end of last year to 5.12% on 30 June 2023. Similarly, Charter Hall Group’s (CHC) average capitalisation rate rose by 32 basis points to 4.8% as of 30 June 2023. Whilst Growthpoint Properties Australia (GOZ) asset values were reduced by 3.6% compared to six months ago, or 7.3% compared to the valuation at the end of FY2022.

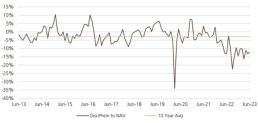

NAV estimates vs AREIT prices (premium/discount)

Source: UBS estimates, FactSet

Clearly the market is still expecting more to come, as the sector as a whole continues to trade at a discount to their Net Asset Value (NAV) as the chart above suggests. However, all this could quickly change if slightly more positive news appears (i.e., stabilising/peaking of interest rate).

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager