As at September 2023

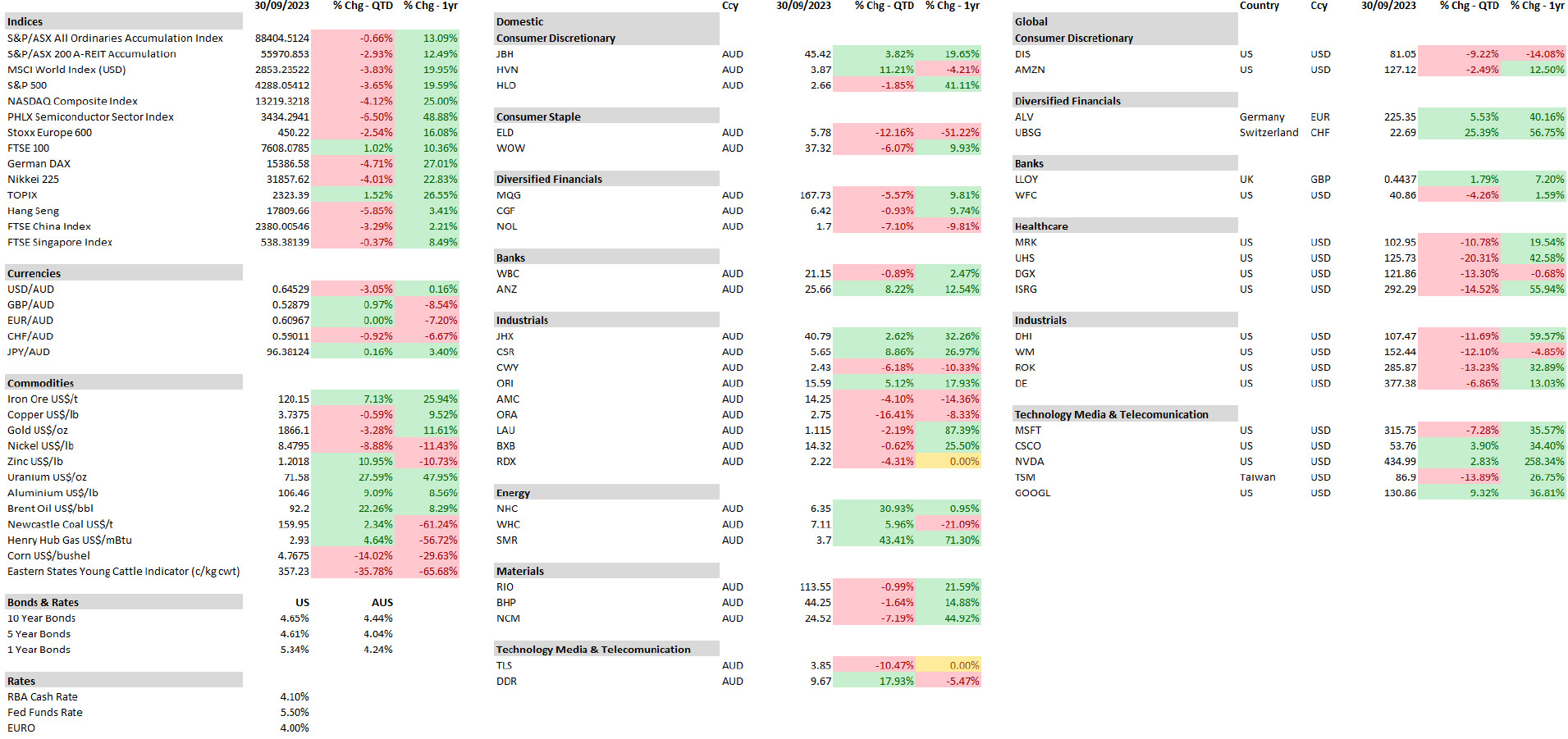

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

As indicated by the table on the preceding page, equities markets advanced strongly over the last year, with the exception of the Chinese market. However, in the last quarter they have retreated to varying degrees as long-term interest rates have continued to rise. Generally, the indices that rose the most have had the biggest corrections. The Nasdaq, and more particularly, the Semi-Conductor Index shown are the most extreme cases.

Amongst the stocks widely held in the portfolios only a handful are down over the year. The situation for the last quarter is not as favourable. While the recent movements have been unfavourable, we think that overvaluation is not extreme or widespread. In cases like Elders (which is covered below in the Domestic section) the fall is a somewhat excessive reaction to agricultural commodity prices and rainfall forecasts.

Declines in commodity prices were largest among those that increased most in reaction to the Russian invasion, that is energy and agricultural commodities. Significantly for the Australian market the iron ore price has held up well, despite Chinese economic issues (the biggest customer). The star performer has been uranium, which is up 48% for the last year, including 27% in the quarter.

Over the year the Australian dollar is little changed against the US dollar; however, it is sharply down against European currencies. The portfolios have relatively little exposure to European stocks, although as an end market for many US companies it is significant.

While central banks have slowed or paused increases in short-term interest rates, bond yields have continued to rise and are now at the highest levels in 15 years (since the pre-GFC levels). Economic growth in developed economies has only slowed very modestly to date and employment levels have remained high (that is close to full employment). Both these factors have led monetary authorities to warn that further action may be necessary. Central banks’ preferred measures of inflation have declined but remain well above the target levels of 2-2.5%. Their view seems to be that rather than a soft-landing, economies have yet to make any landing at all and they remain unconvinced that inflationary pressures are under control. To quote the Federal Reserve Chair, central banks are “navigating by the stars under cloudy skies” (he should try the fund manager’s lot!).

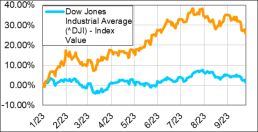

NASDAQ vs Dow Jones Industrial

Source: Capital IQ

Rising interest rates require that we sharpen our focus on valuations. The rise in share prices over the last 15 months has been very large in selected sectors and quite widely spread by industry. Technology stocks rose very sharply, particularly the very large US tech stocks. The insurance and investment banking stocks have also risen sharply, in the case of UBS it was as a result of acquiring Credit Suisse at a huge discount to assets. However, this calendar year a familiar pattern has emerged with the tech sector outpacing all others as is indicated by the chart below. The Orange line is the Nasdaq Index, which is heavy in tech stocks and the Blue line is the Dow Jones, which comprises more traditional industries. Whereas the Nasdaq was up nearly 40% at one stage the Dow is little changed. This pattern was long-lasting prior to covid.

In terms of valuations, the tech sector reached prices that were expensive, but few were truly excessive. Many are excellent companies, with strong revenue growth, high margins and extremely high returns on capital. While we have been reticent to pay the very high prices that have been apparent recently, we are looking to adding to holdings in companies such as Microsoft, Amazon, Nvidia, Google. TSMC is perhaps an exception, and we think the price is quite attractive.

In the last few months three of the portfolio stocks have made large acquisitions, something we are generally very wary of. As mentioned, UBS acquired Credit Suisse, Orora acquired Saverglass and Cisco Systems acquired Splunk Networks. The first was at such a large discount to assets we are more than comfortable that UBS got a great deal. We are also quite comfortable with the Orora acquisition as they have bought a very high-end manufacturer at a very reasonable price. Cisco Systems is probably the most challenging, but we think it looks promising and are willing to give it the benefit of the doubt.

In other sectors valuations are not all that demanding and we are reasonably comfortable in building positions in both the global and domestic markets.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global markets were up 22% over the last 12 months, but down 0.4% for the quarter as measured by the MSCI, an index of global stocks (expressed in A$). As indicated in the overview the big US tech stocks drove a significant part of the return, particularly since the beginning of this year. Microsoft, Google, Nvidia, Cisco Systems and Amazon were all up strongly for the year.

However, there was a large number of sectors that also had high returns over the last twelve months. These included Allianz, which recovered from earlier falls in 2022, and UBS, which benefitted hugely from the acquisition of the distressed Credit Suisse.

Additionally, there were very strong rises in healthcare and in industrials over the last year, despite the falls over the very recent past. In healthcare Merck was up 19.5%, Universal Healthcare up 42.6% and Intuitive Surgical up 55.9%. A holding in Moderna was acquired after very heavy falls from the covid period. The company is best known for its Covid vaccine, but it has a large well-advanced portfolio of oncology and rare diseases drugs. The holding is currently small, but we are looking to increase the position over time.

Despite the sombre mood in the housing industry in the US, homebuilder DR Horton (DHI) rose 59.6% for the year. As we have previously commented DHI is a great company and has had a terrific record over the last 20-30 years. Rockwell Automation which we bought this year is up 32.9%; we think this company will continue to do well as it has a very strong position in the US and a growing global business.

A substantial part of the return has been due to a recovery from depressed prices of a year or so ago. We would not expect such a situation to persist, but neither do we think that the story is over and the underlying returns on capital are still attractive.

A position in John Deere was also added during the quarter. John Deere is the leading supplier of agricultural equipment globally, together with heavy earthmoving machinery. They are widely known for their technology and innovation in increasing the efficiency and productivity in agriculture. The company has very attractive margins, a high return on capital and significant recurring revenue.

The most disappointing sector was commercial and retail banking. Both Lloyds and Wells Fargo did not really participate in the market rises. We had expected an increase in their returns on capital as interest rates rose, however this has been very muted. While the share prices are at very modest valuations compared to their assets, we do need to see an improvement in their returns on capital, particularly in the case of Lloyds.

We might re-iterate the returns on capital that portfolio stocks are earning (with the exceptions mentioned) are extremely high. In particular, the big tech stocks are throwing off extra-ordinary amounts of cash, which they are largely returning to shareholders. For instance, Google is expected to produce in excess of $80 billion in free cash this year and continue to increase that by about 20% p.a. for the next few years. This characteristic is becoming more common among the big tech stocks, which are in effect establishing global monopolies and outpacing their immediate competitors by large margins. We feel it will be difficult for competitors to threaten the dominant position that companies like Amazon, Microsoft, Google, Uber, Nvidia etc have.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Capital IQ

Key focus for the market during the quarter was earnings as companies delivered results for the period ended June 30. The message is corporates are managing relatively well against a backdrop of rising interest rates and soaring cost of living expenses. While segments of the consumer base are struggling, a diverse range of consumer-related companies produced resilient results: grocery retail – Woolworths; discretionary retail – JB HiFi, Harvey Norman; travel – HelloWorld.

Building materials (James Hardie, CSR see previous quarter) also defied sceptics with demand and margins holding up well.

Among commodity stocks, most results reflected lower commodity prices and higher input prices, but on an historic basis, earnings remain elevated.

BHP delivered full year earnings of USD13.4 billion, down from the previous year’s record but, nonetheless, continuing to produce attractive returns on capital – 28.8% on an underlying basis. The iron ore price averaged USD92.54 per ton on a production base of 257 million tons. We note that despite China’s post covid economic difficulties the commodity remains well supported and is currently trading around $120/ton. At these levels, both BHP and Rio are delivering very attractive returns given their cash cost of production around $20/ton.

Full year results for our thermal coal exposure – Whitehaven and New Hope, came in at record levels. This was despite the coal price index retracing significantly from highs experienced following Russia’s invasion of Ukraine. At current prices of around USD160/ton, both miners are doing very nicely off cash cost of production in the $45-55/ton region. A key focus of the market is how each of the producers will manage and deploy their record cash flow: New Hope signals a preference for returns to shareholders while Whitehaven has thrown its hat into the bidding process for two of BHP’s Queensland mines. In each case we remain favourably disposed to our exposures with low valuations and dividend yields exceeding 10% pa.

Although not a core portfolio holding, CBA is an important bellwether stock for the banking sector as well as for the wider economy. The read through from its full year results is that the bank is delivering modest single-digit earnings growth off the back of reasonable lending growth (mortgages +5%, business + 11.4%), but cycling against margin pressure as the net interest margin peaked in 1H’23 before declining 5 basis points in the second half. Credit quality of the loan book remains benign with little evidence to date of significant distress despite higher interest rates. From an investment perspective, our chief concern remains valuation against expected returns on equity. Overall, we remain underweight the sector with a skew toward cheaper priced ANZ and Westpac.

Despite our positive view of Elders (see previous quarter’s comment) the stock has continued to fall and is now back to prices last seen in 2019. Our position remains unchanged: the quality of the business has improved significantly under the leadership of Mark Allison, taking a level of cyclicality out of earnings through diversification into new business segments and new geographic regions. If climatic conditions do worsen, as many fear, this diversification strategy places the company in a better position; near term risks to earnings are captured in current valuations. Viewed through the cycle, we expect the company to continue delivering attractive returns to the equity holder.

In the period our portfolios have held packaging company Orora, we have been impressed with the strategic decision making of the management. Following the sale of its low-returning fibre packaging business, the company returned approximately $1billion to shareholders in dividends and share buybacks. This left the company focused on higher margin bottles and cans in Australia and higher growth packaging solutions in the US. To this has now been added, through acquisition, French company Saverglass – a global leader in design and manufacturing of high-end bottles to the premium spirit and wine markets. The transaction, valued at $2.2billion, is expected to be earnings accretive in the first full financial year of ownership (FY24/25). We will have further to say on this transaction in the periods ahead but our conclusion at this point is that Orora has acquired a high-quality manufacturer at an attractive price, providing the company with a third platform for growth. PPM will participate in the company’s $1,345million capital raising.

Finally, Redox was added to the portfolios as it listed on the market from private ownership; market capitalisation approximately $1.2billion. The company is a wholesaler of chemicals, plastics and other ingredients, servicing over 6,400 customers across a diverse range of industry sectors including industrial, household, personal care, human health, and agriculture.

The company has a family heritage and has a long history of organic and inorganic growth in a fragmented industry. The company has been able to deploy capital at a consistently high rate of return, with prospects of this continuing as it takes advantage of a fragmented industry; Redox has a market share of approximately 4%.

Redox is also in the early stages of expanding into the much larger US market. Although we would not ascribe significant value to this business at this stage, we do see potential to leverage off its existing business, in particular the global supplier network and data analytical capability.

Interest Rates

Ian Hardy

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

Across the globe, central banks are maintaining their longer-term targets of 2 to 3% inflation and with inflation stubbornly above this, rates are expected to remain higher for longer.

At its most recent meeting the US federal Reserve (The Fed) noted that it remains “highly attentive to inflation risks” and maintained the target range for the federal funds rate at 5.25% to 5.5%. In addition, it will continue reducing its holdings of Treasury securities as set out in its previously announced plans. At the time of writing the yield on US 10-year bonds was 4.80%, the highest level since 2007.

In the UK, the Bank of England ‘s Monetary Policy Committee (MPC) maintained the Bank Rate at 5.25% and “judged that the risks around the modal inflation forecast were skewed to the upside,” while GDP growth is likely to be weaker than expected.

At the September meeting of the European Central Bank (ECB), the release commented that “inflation continues to decline but is still expected to remain too high for too long” and accordingly raised rates by 25 basis points.

In Australia, the Reserve Bank (RBA) left rates unchanged at 4.10%, at its first meeting under new Governor Michele Bullock. The RBA considers “recent data is consistent with inflation returning to the 2-3% target over the forecast period.” However, with a tight labour market and high levels of capacity utilisation this may prove difficult. The final sentence of the RBA Statement, reads, “the Board remains resolute in its determination to return inflation to target, and it will do what is necessary to achieve that outcome.”

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Capital IQ

The A-REITs sector had a strong start to the quarter, rising approximately 6% up to the end of August. However, these gains evaporated in September with the index finishing down 2.93% for the quarter. The rise in bond yields negatively affected the sector, reducing property valuations.

A key differentiator between operators was the ability to pass through inflation increases to rent increases. This was partly offset by higher borrowing costs for those that had debt maturities. The rise in borrowing costs we think will eventually flow through to all borrowers as it seems unlikely, we will return to the near zero rates of the covid period.

Property with favorably structured leases, enabling them to pass on inflation increases, tend to be in Industrial, Storage, Land-lease and certain sectors of the Retail space, where values are more likely to see support.

The Office Sector continues to be the most adversely affected sector. Large vacancy rates in CBDs have seen pressure on rents and increases in incentives. Discovery of real valuations remains challenging with very few transactions and a large buyer-vendor spread. A few large office assets remain on the market whilst others have been removed from the market or remain in negotiation with cautious buyers.

Residential developers like Mirvac (MGR) and Stockland (SGP) are in a more attractive situation. Both MGR and SGP point to the acute undersupply in residential markets. Supply remains constrained, with demand being supported by strong population growth. The shortage of housing is a positive catalyst and will take many years to correct, creating a potentially positive medium-term earnings growth outlook for these residential developers.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager