As at December 2023

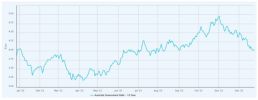

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

Equity markets rose strongly over the last twelve months. Bond yields have fallen, and central banks are signalling lower short-term rates at some time this year. Inflation has also fallen from high levels twelve months ago to close to central bank targets.

Our view is that equity valuations, while not as attractive as they were 12-18 months ago, are not excessive in many industry sectors. We think that after a difficult period, company profitability is generally improving, and this is a positive sign for equities. The subsidence of inflation indicates lower short-term rates, but not so much so for bonds, where yields have already fallen.

As can be seen from the table on the preceding page, equities markets advanced strongly over the last year. The domestic Australian market was up 13.0% and the global markets were up 21.8%. Markets except for the Chinese market and the UK were up strongly, this was particularly the case for technology stocks, although the increases occurred in the first half of the year and the sector was only up marginally from mid-July.

The Australian dollar was slightly up (+0.3%) against the US Dollar during the last twelve months finishing the year at 68c, which is at the lower end of the band in which it has traditionally traded. Against the Japanese yen the A$ was up 7.2%, but down sharply (-5-8%) against European currencies.

Interest rates rose during the year with the RBA raising short-term rates from 3.10% at the beginning of the year to 4.35%. The Australian 10 Year Bond yield rose slightly from 3.73% to 3.96%; the difference reflected a change in market views on the direction of interest rates during the year. At the beginning of the year central banks made hawkish comments about staying the course until inflation was beaten, but by the end of the year the rhetoric had softened. Importantly, the Federal Reserve signalled reductions in 2024, although it is by no means certain that this will occur early in the year, as seems to be the market’s current view. We anticipate that other developed country central banks will follow but not necessarily with the same timing. Inflationary fears have moderated over the last twelve months and are now approaching central bank target levels.

The Australian listed property index rose 17.6% for the year, recovering from a fall of 20.1% the previous year. Nearly all the return occurred from the end of October and coincided with the sharp fall in bond yields.

The price of energy commodities fell sharply during the quarter and for the year, with the exception of uranium, which was up 27% and 90% for the respective periods. The iron ore price continued to rise and was up 17% in the last quarter as did copper (another key commodity for portfolio stocks). Agricultural commodity prices fell from very high levels of 1-2 years ago, but importantly for Elders, a major holding in the portfolios, the cattle price rose significantly; the prediction of dry conditions seems to have been a little premature!

In the September quarter we pointed to the strong rise in equities markets over the prior twelve months but noted that valuations had not become excessive in many sectors outside technology.

Indicative of a change in sentiment over interest rates, there was a marked change in the prices of consumer related stocks and particularly those related to residential construction. Domestically, James Hardie and CSR were up 38% and 17% respectively; DR Horton, a US homebuilder, was up 41%. Related to homebuilding, JB Hifi and Harvey Norman were up 16.8% and 7.5% for the quarter.

After the sharp falls in agricultural commodity prices, we have been adding to positions in stocks such as Elders and Deere and Company in the US. We think that the sharp falls in both companies’ share prices offers an opportunity to access long-term attractive returns on capital at attractive prices.

The finance sector had mixed returns, with poor performances in Australia and the UK, particularly in stock with high exposure to residential lending. We have re-thought our views on this type of lending and now do not expect to get the very attractive returns that were produced in the decades before the GFC. Margins are low and have not recovered as might have been expected with the rise in interest rates.

While prices are not as attractive as they were a year ago when there was considerable concern about the prospect of a recession, we do however think there are opportunities to buy companies that generate a high return on capital at attractive prices. Although we must be more discerning now, we would note that market advances tend to last for quite long periods, and this is a relatively early stage in the cycle.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global markets rose 23.4% for the last twelve months, as measured by the MSCI (an index of global stocks) in A$ terms, and 11.4% for the last quarter. It is worth noting that this widely used global index has again become dominated by US stocks, which in turn are dominated by a very small number of technology stocks. In the index, the US stocks make up 70% of value and the 7 big tech stocks make up nearly 20%.

The global stocks in portfolios had a strong year across a range of sectors, with Technology, Industrial, Consumer Discretionary and Financials (except Lloyds) all up strongly.

We have been through a process of reducing holdings in some of the stocks where valuations are difficult to justify. As a result, we disposed of most of the holdings in Nvidia in the last six months. The company has a dominant position in the design of chips for artificial intelligence (AI) and more generally for data centres where there has been an explosion in demand for computing power. However, there is a limit to the price that can be justified – new portfolios or money has not been invested in this stock at recent prices. We feel that this is a great company, and we would invest again at lower prices. We are being cautious in reducing the holdings in these companies as we view them as having very long-run growth opportunities.

We are continuing to invest particularly where prices have been depressed by what might be regarded as short-term unfavourable developments. In this regard, we added to holdings in Deere & Company during the quarter. While the company has indicated conditions in the agricultural sector will be more difficult this year, we feel the declines in price more than reflects a cyclical downturn. The company generates an attractive return on capital.

Another sector that has lagged the market is healthcare, which picked up during the quarter, but overall had a difficult year.

As mentioned in the last quarterly report the portfolios acquired a holding in Moderna, best known for its Covid vaccine, but which also has a rich pipeline of drugs under development. We feel that the fall over the last two years from over US$450 to below US$100 has taken the hype out of their Covid success; it is widely understood that the massive revenue stream from Covid vaccines would fall very substantially in future years (but by no means disappear). Covid provided Moderna with approximately US$20 billion in earnings over 2 years, which has allowed them to fund a significant research program (and buy back a lot of stock). One of the most interesting developments this quarter has been the success of a Moderna’s cancer vaccine in a trial with Keytruda (the Merck blockbuster oncology drug). These vaccines are not prophylactic, like Gardasil, but rather an adjunct, in this case to Keytruda; survival rates in the 3-year trial were 50% higher than for Keytruda alone. Moderna has now commenced trials for other cancer indications – success would be significant for both Moderna and Merck.

In the last quarterly report, we flagged some concern over the returns being generated in areas of the finance sector. We have trimmed our holdings in banks whose primary line of business is residential mortgages; in the global portfolio this is Lloyds. We are retaining Wells Fargo as the margins have picked up and their business is less dependent on residential mortgage business.

Despite the strong rises in markets over the last year, the concentration of the return in a narrow range of stocks presents opportunities to invest in areas that are less fashionable. Valuation however is critical, and we are being cautious after recent rises.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Capital IQ

The Australian equity market reached a calendar year low of 6,980 in late October as investors showed concern over the level of inflation and interest rates. Clearly of surprise has been the subsequent moderation of price rises, here and overseas, and the resultant fall in market interest rates. This precipitated a strong year-end rally, led by interest rate sensitive stocks as well as some recent underperformers.

Whitehaven Coal was confirmed as the successful bidder for two of BHP’s metallurgical coal mines in North Queensland. In what is a transformational deal, WHC will pay USD 3.2 billion for the Daunia and Blackwater mines, in the process significantly expanding production capacity. In our view the acquisition was made at an attractive price multiple and will be immediately earnings accretive. Commodity prices are inherently volatile, but this price level appears to capture a significant part of any pricing risk.

The deal will transform the company from a predominantly thermal coal producer to majority (70%) metallurgical coal producer, while delivering a significant uplift in the company’s resource base. Annual production will rise from 13 million tonnes to around 33 mt. The stock valuation remains attractive, trading on a PE multiple of around 5.4X FY25 earnings, the first-year post-acquisition.

Agriculture stock Elders delivered its FY23 results, which were in line with market expectations. It’s reflective of the generally negative view of the market that although it was an in-line result the stock surged 18.2% on the day of the announcement. Despite earnings before interest and tax falling 26% due to softer livestock and ag-input prices, the result was the second highest in Elders’ history. This, in our view, demonstrates a resilient business operating across a wide geographic footprint and which continues to execute on its growth opportunities, both organic and inorganic.

Our simple conclusion is that the company has a record of delivering high returns even during the most challenging of climatic conditions. This does not seem to be well appreciated by the market, providing an opportunity for the equity investor.

Orica, which produces explosives and related services for the mining and construction industries, also delivered results during the period. The company has been cycling a difficult few years as remediation work was undertaken on its important Burrup ammonia nitrate facility in Western Australia. Equipment faults have hampered the company’s ability to further expand market share in the WA iron ore region. To meet existing contracts, the company has had to supply AN from its east coast production, but at a lower margin than would otherwise have been the case.

Positively, the company has progressed past this period and is seeing a recovery in earnings and returns on capital. Demand from end users, particularly among the miners, remains strong. Underlying earnings before interest and tax jumped 24%, also helped by improved contractual conditions. With a positive demand environment and attractive market structures, we view prospects for further improved results to be positive.

We have made comment previously that competitive pressures in the banking sector have been weighing on the ability of banks to expand lending margins. The experience of the three banks (ANZ, NAB, WBC) reporting in the quarter adds to this picture and confirms our underweight position in the sector. Structural change in the industry would suggest that this position is long term in duration.

James Hardie produced record quarterly income on the back of strong pricing in its core North American market. The company has an outstanding record of delivering growth above market while maintaining high levels of profitability. It helps that JHX has an effective monopoly in its product category (fibre cement cladding), a product in consistently high demand. Company guidance for next quarter came in 30% above market expectations, resulting in the share price once again closing in on its record high level. This is a stock that continues to deliver.

Overall, we are comfortable with the weighting of the domestic portfolio. Our focus on value has helped navigate a difficult market. Repositioning away from major sectors with challenges – banks, towards areas with better opportunities such as logistics – Lindsay, Redox, is part of a continuing process.

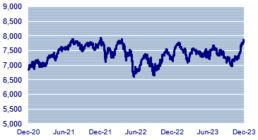

Interest Rates

Ian Hardy

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

Interest rates have been headline news for most of the last two years, especially in Australia where the official cash rate has risen from effectively zero to 4.35% currently, as the Reserve Bank of Australia (RBA) attempts to bring inflation back to its preferred 2% -3% band. The RBA is clear in being data driven on its interest rate settings but at this juncture the data is far from clear. This is particularly the case with events in the Middle East and Russia/Ukraine driving commodity prices. Interestingly, the RBA has been restructured by the Labor Government and the external board members will dominate decisions in future and only meet eight times a year.

In the United States, the Federal Reserve has indicated that it thinks rates have peaked. At its last meeting of the year, the FOMC held the Federal Funds target unchanged at a range of 5.25-5.5%.

Around the world major central banks held rates steady with Bank of England maintaining the Bank rate at 5.25% and suggesting it will remain at this level until Q3 this year. The Bank of Canada held its benchmark overnight rate steady at 5.0% and softened its tone, stating that recent data suggest “the economy is no longer in excess demand.”

In Europe the European Central Bank (ECB), decided to keep interest rates unchanged despite a drop in inflation in recent months, as “it is likely to pick up again temporarily in the near term.”

In summary, it would appear inflation and hence interest rates have peaked but will not begin to reduce until the latter part of 2024.

Despite the caution that central banks are showing in reducing short-term rates the bond market yields have reduced significantly. From Late October yields have fallen by approximately 1%. Whether this optimism about the rate of official interest rate reductions is misplaced is yet to be seen.

As an observation, it might be noted that the Federal Reserve is no longer providing the same support to the bond market that it has for over a decade. In its last meeting it reiterated its intention to reduce its holdings of Treasury securities. It had become the largest buyer of government debt, increasing its balance sheet to approximately $9 Trillion. Under the policy implemented 18 months ago the mountain has been cut by about 18% – still a long way to go to get back to the pre-GFC level of $1 Trillion.

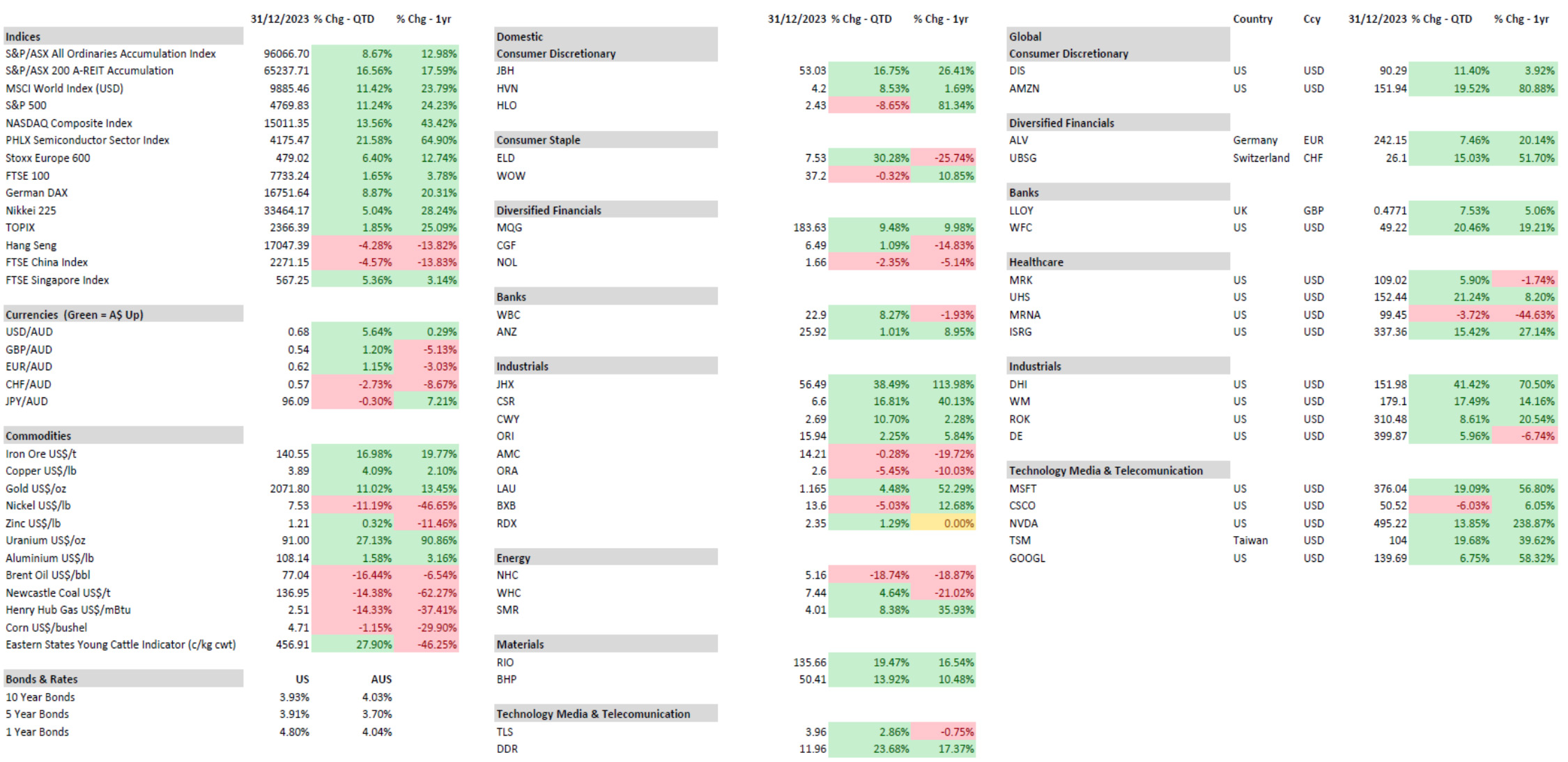

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Capital IQ

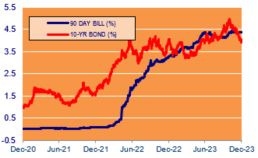

The Australian listed property sector has had a difficult period ever since the RBA started increasing interest rates in 2022. After a big decline in calendar year 2022, the Property Index (A-REIT) was on track to post another large decline in the first 10 months of 2023. However, with the decline in bond yields from the end of October (see chart below), the Index rallied to post a 17.6% return for the year.

Australia 10 Year Government Bond Yield

Source: S&P Capital IQ

There has been a wide divergence in operating performance for different parts of the property sector during the year.

We have seen improvement in the operating conditions across retail property stocks. HomeCo Daily Needs REIT (HDN), owner of a portfolio of neighbourhood shopping centres, reported healthy foot traffic, a very high occupancy rate, and good growth in rental income. HDN’s guidance for its FY24 dividend is 8.3 cents per share, which gives it a yield of 6.7% at the current share price.

Large format shopping centre owners like Scentre Group (SCG), which owns the Australian Westfield shopping centres, and Vicinity Centres (VCX) reported similarly strong trading results. These large shopping centres are in very good locations and very hard to replicate. The leases typically have inflation linked annual rental escalation clauses attached, which should support and grow their dividends which currently are yielding around 5.7%.

Demand growth for Industrial property is moderating while businesses reassess floor space requirements as the supply chains continue to normalise. Industrial property in Perth and Adelaide has seen rental growth stalled. However, major cities like Sydney, Melbourne, and Brisbane appear to be more resilient and continue to experience strong rental growth as vacancy remains very low.

We remain concerned about returns for the Sydney and Melbourne CBD Office sectors. New supply coming into the market in the next couple of years is still outpacing demand growth, and the oversupply situation may take a number of years for the market to digest. Although it is true that A-Grade office buildings have typically fared better during downturns, Dexus (DXS), which is the largest office property owner, is still experiencing a deterioration in their occupancy levels which stand at 94.7%, down from 95.9% previously. This is far better than some others that have lower than 90% occupancy.

Outside the Sydney and Melbourne CBDs, office property seems to have fared better. Occupancy for Elanor Commercial Property Fund (ECF), which owns office space in the Gold Coast, Canberra, Brisbane, and on the fringes of Sydney and Perth’s CBD, remains high and pressure on rents is less apparent. Property assets are valued conservatively with an average capitalisation rate of 6.95%. ECF gave guidance of distributions of 8.5 cents per share (yield of 11%).

As interest rates rose (particularly long-term Government Bonds) to end October, listed property became less attractive. But with Government Bonds now back to 4%, we feel the A-REITs with an average capitalisation rate of around 6% may provide an attractive alternative for investors looking for income.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager