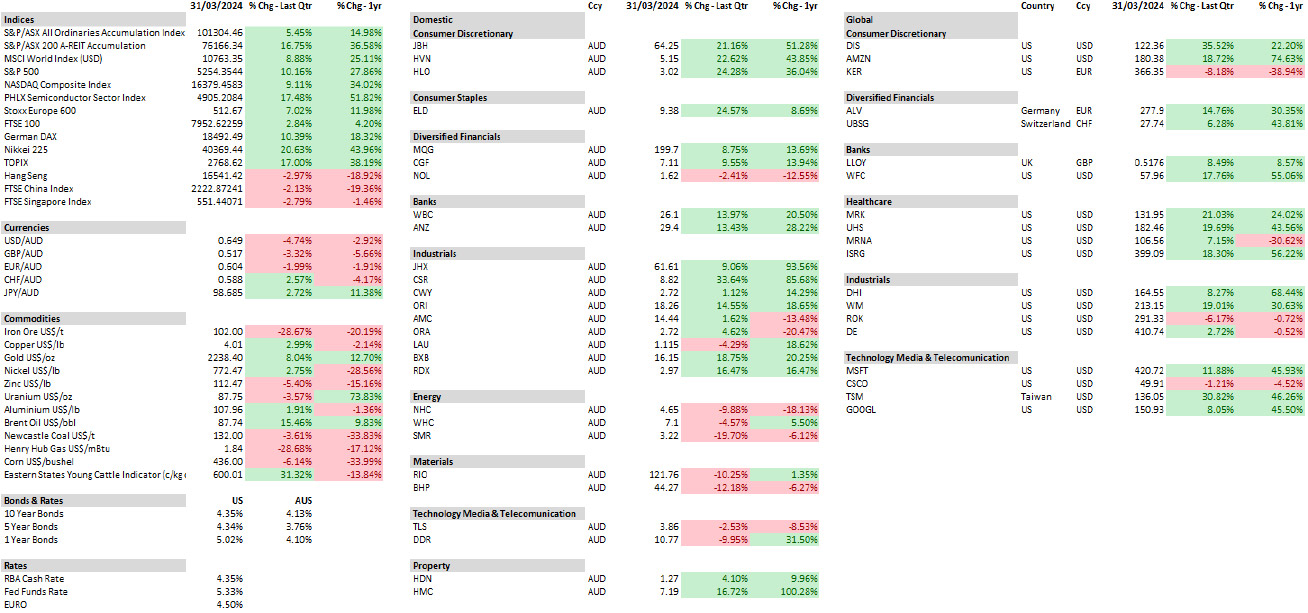

As at March 2024

Equity Market Returns

Source: Capital IQ, MSCI

Overview – Hugh MacNally

Equities markets rose strongly during the last 12 months, the MSCI (a global Index) was up 25.1% and 8.9% for the quarter ended 31 March 2024. Since the equities markets bottomed in September 2022, two and a half years ago, the MSCI has risen approximately 40%. Stock Indices returns over the last 12 months have varied widely: the Nasdaq and Philadelphia Semiconductor Index were up 34% and 51% respectively, the Japanese market was up 44% and the Australian Property index up 37%. European markets were up a modest 12% and the UK market a mere 4%. Not surprisingly the Chinese markets fell sharply, down close to 20%; declines have now been going on for four years in these markets, which is a long time in any market reflecting the severe problems in the real estate markets and concerns over Party involvement in the technology sector.

After declining 30% over the last two years the Australian property index rose 16% in the last quarter. The rise largely resulted from the expansion of data centres by the Goodman Group.

The Australian dollar fell against major currencies, other than the Yen. Commodities were generally weak although some recovered in the latest quarter (please see Data Sheet). The standout exception was Uranium which was up 74% over the last 12 months.

Speculation is rife on when interest rates will be reduced by central banks, however, this is starting to have less of an impact on equities markets. During the quarter, while bond yields increased over 0.75%, equities markets were up strongly. Greater focus seems to have shifted to earnings growth and the developments in technology and artificial intelligence (AI). The latter has been one of the major drivers of equities markets returns over the last two years.

As is covered below, the earnings results from a wide variety of industries have been encouraging and in many cases from industries that might have been expected to be under pressure from increased interest rates, such as housing construction, consumer discretionary spending and the banking sector.

The observation we would make is that interest rates are not that high by historical measures, and that in the past economies have been able to grow at satisfactory rates with interest rates at similar levels to those that currently exist.

After such a sharp rise in equities we felt it was important to review stock valuations. We take a long-term view and don’t want to sell out of stocks that have very long-term growth opportunities unless their valuations are so high that the expectation holds unacceptable risk. We felt that this situation had been reached with Nvidia, a great company, but we could no longer justify the price. For different reasons, Waste Management Inc was sold, another great company but with very much slower growth. There were less of the valuation related questions for stocks in the domestic Australian market.

The question of valuation also applied to the banking sector. For the twenty years leading up to the GFC the returns from banking stocks were extremely high, of the order of 20% p.a. and they were often a very large part of portfolios. However, due to the effects of regulation, higher capital requirements and some structural changes to their markets; the returns are much diminished. The price recoveries in the last six months have provided an opportunity to reduce the positions, which we now regard as less likely to provide us with the long-term returns we require.

International Equities

Hugh MacNally

International Equities Performance

Source: MSCI

Global equities markets rose strongly during the quarter ended 31 March. The MSCI was up 25.1% for the year and 8.9% for the last three months.

The equity market returns were achieved in spite of growing scepticism of an early interest rate reduction in the US. After initial early gains in the fight against inflation, returning the core measure to central banks’ target has proven to be more difficult than was expected. However, the current level of interest rates does not seem to be much of an impediment to economic growth or the growth in corporate earnings.

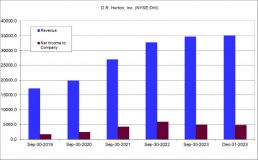

Looking at what might be regarded as one of the most interest rate sensitive areas, housing construction, the response to higher rates has been very muted considering mortgage rates have gone from under 3% to over 7%. Housing starts are slightly up on the level a year ago. House builders do not seem to be suffering a lack of demand in the US and other developed economies. The chart below shows the revenue (in Blue) of DR Horton, the largest home builder in the US, which has grown an average of 17% p.a. over the last four years and while growth has slowed the absolute level has not dropped. The bars on the far right are for the 12 months to 31 December 2023. Profitability has grown even faster at an average of 29% p.a. These results would not suggest that the consumer is stressed.

Source: Capital IQ

There is a similar picture of growth in consumer staples, which is in line with historical norms. Additionally, non-performing loans in the banking sector indicate a benign environment, with non-preforming loans slightly below the levels of three years ago and substantially below those of 6 or 7 years ago.

We think that the above indicates that growth in corporate earnings is not reliant on reductions in interest rates, which, as were pointed out earlier, are not unusually high by historical standards.

While in many industries operational conditions seem reasonably favourable, in the tech sector the growth has been explosive. This has been particularly the case in software and chip manufacture and design related to AI (Artificial Intelligence). The seven largest tech stocks have had strong revenue growth in the range of 10% to 30% in the last year – the outlier was Nvidia where revenues grew by over 200%. Earnings for the sector have grown at substantially higher rates and have exceeded the growth rate of the rest of the market by an order of magnitude. We see no reason why strong growth should not continue given the magnitude of the change that is occurring. The question that is difficult to answer is what price one should be willing to pay for this growth.

It is not only in the tech sector that strong earnings growth is occurring. One of the companies we have put in portfolios during the quarter is United Rentals, which operates a US nationwide plant and equipment rental business. It currently has approximately 17% market share in the US. Growth in revenue over the last 5 years has averaged 12.2% p.a. and earnings per share has averaged 22%. These are very attractive numbers. The growth has come from strong construction and infrastructure spending. There has also been consolidation in the industry for which United is well placed to benefit. The company is not expensive in our view.

After an extended period of difficult operating conditions, the finance sector has had a very strong year. Wells Fargo, UBS and Allianz all had strong rises: the two banks share prices increased approximately 50% for the year and Allianz was up 35%. While the share price rises were large, we are as yet to be convinced that they are anything more than a recovery from depressed levels. The critical measure, the return on their shareholders’ capital, is still low. Wells Fargo we think is the best placed to achieve improvements, but they are not there yet.

Merck & Company had a good year for growth in their medicines outside those related to Covid-19 where revenues grew 9%. In particular Keytruda’s revenue, their massive blockbuster, was up 22%.

With the strong rise in share prices over the last 12 months we have been looking at the valuations more closely and we have reduced or sold several companies where the valuations do not make sense. Fortunately, we have been able to re-invest in some great companies that have remained attractively priced.

Australian Equities

Peter Reed

Australian Equities Performance

Source: Capital IQ

Since bottoming in October ’23, the Australian equity market has followed the lead of global markets higher. Banks led, followed by discretionary retail, offsetting losses from the materials sector.

Grocery retailers attracted their share of attention as cost-of-living pressures continued to bite and with the issue moving into the political sphere. Our portfolios have for a time maintained a core position in Woolworths, which was established when the incumbent grocers were under significant pressure from hard discounters such as Aldi and Costco.

Our view was that the discounters would be able to build a market share, based on their low-cost, narrowly focused business model, to say around 10%. After that, further market share gains would be much more difficult to attain since they would have to compete in wider product categories, complicating logistics systems and adding to their cost base.

In the meantime, our expectation was that Woolworths would reset its position, sharpen its focus, and compete more effectively against the newcomers. Under then newly installed CEO Brad Banducci, this is exactly what happened with the retailer getting its “rhythm” back and delivering improved operating performance. Shareholders were rewarded with a doubling of the share price from 2016 to 2021.

This brings us to the present and one of the more notable actions in the portfolio during the quarter was the decision to exit our Woolworths position. Share price gains by the stock meant that it was no longer positioned in the highly attractive value range that it once was. Further, there were concerns which had built over a period in terms of its strategic direction: acquisitions had been made into adjacent areas, such as pet food and food delivery, while exiting its strong position in alcoholic beverages (Dan Murphy, BWS).

We have always viewed the grocery retailers as having long business cycles. Woolworths appears to be closer to the top of its cycle, and so we will sit on the sidelines for a period. We may have an opportunity to reinvest again at some point in the future but this, of course, will be dependent on pricing and operating performance.

Staying within the retail space, discretionary retailers JB HiFi and Harvey Norman, as well as travel company Hello World, delivered strong first half earnings results. In the case of Harvey Norman, while the company performed strongly in the early stages of Covid – consumers were confined to their homes, encouraging spending on household good and appliances – coming out of the pandemic the company cycled through several years of weaker revenue and earnings. This was to be expected, given the temporary nature of government and central bank stimulus, but what has been pleasing to see is that as conditions normalise, revenues and profits have settled at a rate comfortably above pre-pandemic levels. In the company’s domestic franchise segment, for example, revenue and profit remain 15% above the 1H 2020 level. At its current stock price, the company offers return potential above our 10% hurdle rate.

Noble Oak, our domestic life insurance exposure, continues to successfully execute on its business strategy. First half results indicated that its key operating metric, in-force premiums or outstanding policies, grew 24% in a market growing circa 3%pa; active policies stand at 128,000. This delivered the company a market share of 3%, up 0.5% since December 2022, with plenty of growth opportunities remaining. Through its direct marketing channel, in particular, the company has been steadily adding alliance partners with well-known names such as Budget Direct, Costco and CPA Australia. All up, Noble Oak has over 40 alliance partners, providing a large distribution base which can be efficiently accessed.

The company has a strong capital position with a capital adequacy of 228%, sufficient to support its organic growth. During its strong growth phase, we recognise the company is capital hungry, but as it reaches a level of maturity over the next three to four years this position should ease, allowing greater scope for shareholder distributions. At a prospective price earnings multiple of less than 7 times, the stock valuation cannot be considered to be stretched.

We have kept a cautious view on the banking sector. We view CBA as being at an extremely high valuation at 3 times their book value. Valuations for the other major banks are also somewhat stretched given share price outperformance during the quarter. Investors appear to have focused on the banks’ capital positions as well as solid loan books, with low levels of bad and doubtful debts as an indicator for future dividend distributions.

Valuations of the cheaper banks (ANZ and Westpac) are more palatable than CBA but given they trade at a premium to their book values, along with a return on equity either side of 10%, an underweight position is warranted. What would change our stance on the sector would be if we were to see higher returns on capital off the back, for example, of expanding net interest margins. However, given changes in the structure of the market (stronger role of the mortgage brokers) as well as currently unabated competition among the lenders, prospects of this appear limited for the time being.

Interest Rates

Ian Hardy

90 Day Bank Bill (%) vs 10 Year Bond (%) Performance

Source: Capital IQ

Interest rates remained newsworthy over the quarter with Central Banks around the world, led by the US Federal Reserve, talking down the number of future rate reductions. The Federal Open Market Committee (FOMC) held the Fed Funds rate steady at 5.25-5.50 percent, while projecting 0.75 percent cuts by the end of the year. The latest statement from the FOMC repeated that it is watching for greater confidence that inflation is sustainably moderating toward its 2% target before reducing rates.

In the UK, the Bank of England kept the Bank rate unchanged at 5.25% at its last meeting for the quarter saying that “the economy is not at a point where the Monetary Policy Committee (MPC) can start cutting rates, but the economy is moving in the right direction.” In common with the US Fed the MPC needs more evidence of moderating inflation before beginning to cut rates. This may not happen until the second half of 2024.

The Reserve bank of Australia (RBA) has continued to hold the cash rate steady at 4.35%, although the March minutes confirm that it is moving closer to a neutral stance. The very strong February labour market data suggests that rates will be on hold until well into the third quarter of 2024 even though inflationary pressure elsewhere in the economy does appear to be easing.

Just to be different the Bank of Japan has moved rates from negative to positive as deflation finally comes to an end in Japan.

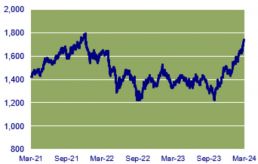

Property (REITS)

Franklin Djohan

ASX Property Graph

Source: Capital IQ

After declining 30% in the last two years, the property index significantly outperformed the broader All Ordinaries Accumulation Index, registering a 16.2% return for the quarter. The majority of listed property stocks had a strong March quarter. Shopping centre owners Scentre Group (SCG) and Unibail Rodamco (URW) experienced strong gains. Similarly, property fund managers Charter Hall Group (CHC) and HMC Capital Limited (HMC) both registered gains of 14% and 16.7%, respectively.

The largest contributor to the property index during the quarter was Goodman Group (GMG). GMG was up 33.6% during the quarter, and with the company’s market capitalization comprising over a third of the property index, it accounted for around two-thirds of the index’s return. The company reported strong results during the quarter and also upgraded its full-year guidance for FY24. The company is branching out from its traditional industrial properties into Data Centres, expanding its data centres pipeline to 4GW (data centres’ capacity is measured by their energy consumption – note to Energy Minister, they need to operate 24/7) across 12 major global cities. Data Centres under construction currently represent approximately 37% of the total $12.9 billion of Work in Progress. On the negative side, the company is not immune to cap rate expansion, with cap rates expanding by 60bps to 5.1%, which impacted assets under management (AUM). GMG trades at a substantial premium to net tangible assets, while most of the REIT (Real Estate Investment Trust) sector trades at discounts to NTA (Net Tangible Assets).

Healthco Healthcare and Wellness REIT (HCW) was one of a handful that were down, with the stock dropping 13.6% for the quarter. One of HCW’s large tenants, Healthscope, is in the middle of a corporate restructuring process with its lenders. This has put pressure on HCW’s share price as there is concern that the landlord will need to provide some sort of rent relief.

PPM is continuously looking for ways to improve the service we provide to you and your feedback is important to us. We hope are staying safe and healthy. Please contact Jill May, Head of Client Relationships with any questions, comments or suggested improvements at jm@ppmfunds.com or on (02) 8256 3712.

Private Portfolio Managers Pty Limited ACN 069 865 827, AFSL 241058 (PPM). The information provided in this document is intended for general use only and is taken from sources which are believed to be accurate. PPM accepts no liability of any kind to any person who relies on the information contained in this document. The information presented, and products and services described in this document do not take into account any individuals objectives, financial situation or needs. The information provided does not constitute investment advice. You should assess whether the information is appropriate for you and consider talking to a financial adviser before making any investment decision. Past performance is not necessarily indicative of future returns. © Copyright Private Portfolio Managers Pty Limited ABN 50 069 865 827, AFS Licence No. 241058.

Your Investment Management Team

Hugh MacNally

Portfolio Manager,

Executive Chairman

Peter Reed

Portfolio Manager,

Director

Franklin Djohan

Portfolio Manager / Analyst

Max Herron-Vellacott

Portfolio Manager

Neil Sahai

Portfolio Manager