Covid-19 clusters anticipated – but moving to re-open economies

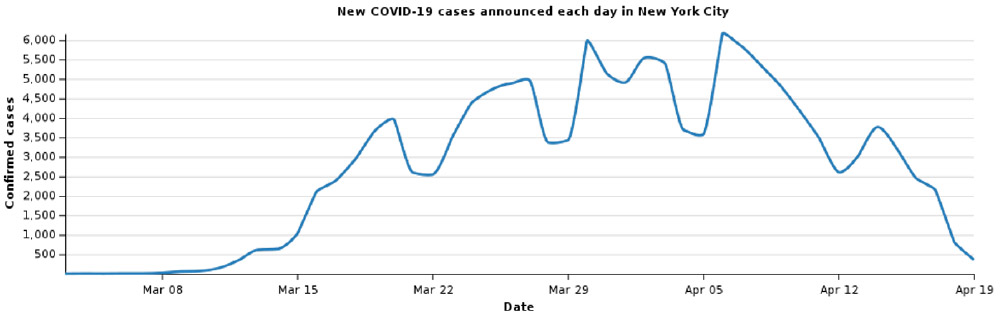

The viral infections now seem to be appearing as spot clusters and seem to be following an established path. Below is a graph showing the reported new infection numbers in New York, which was two weeks ago one of the hot spots. Because of the very limited extent of testing it only shows the more severe cases not the asymptomatic or mild cases where individuals were either unaware they were infected or symptoms were so mild they did not present themselves. No large scale study has been done to measure the true extent of infection, but small studies (which have significant limitations) indicate that the infection rates may be many multiples of the reported numbers and that asymptomatic cases may make up 40-50% of all cases. This would go to the level of herd immunity which has developed.

There has been a gradual lifting of restrictions and a limited resumption of activity. Should this continue to go well then economic activity may pick up more quickly than had previously been thought. This is of great importance as it will limit the liquidity strains on businesses and individuals and consequently the extent of financing required by governments (which is in our view a long-term concern).

There has been a gradual lifting of restrictions and a limited resumption of activity. Should this continue to go well then economic activity may pick up more quickly than had previously been thought. This is of great importance as it will limit the liquidity strains on businesses and individuals and consequently the extent of financing required by governments (which is in our view a long-term concern).

Quarterly reports are starting to come out in the US and these are showing dramatic reductions in earnings. We would expect that this will continue, with some exceptions, such as grocery and some online businesses such as Netflix and Amazon, for this quarter and the next. There will be little good news, but this is universally accepted. The extent of the earnings decline cannot be reliably estimated so we cannot be too complacent about share prices. There is wide conjecture about what shape a recovery might take but at this point the view is U shaped. We tend toward this view also.

To date the earnings reports have been in the finance sector and while earning has been sharply lower than previous quarter and mostly also against previous corresponding quarter there are no signs of balance sheet issues. As we have stated earlier, these companies went into the crisis with very strong financial structure in contrast to the 2008 financial crisis. If the view above proves correct we would expect that this sector will emerge in relatively good shape and in contrast to what the large falls in share prices would suggest.

Similarly, the core holdings in the portfolio, having strong financial positions, will also emerge well. It would be expected however that the earnings reports for most will be well below those of the last period of last year. Even in defensive areas such as healthcare and pharmaceutical we would expect pressure on earnings. We think that much of this is priced in the market.

Kind Regards,

Hugh MacNally

Chairman